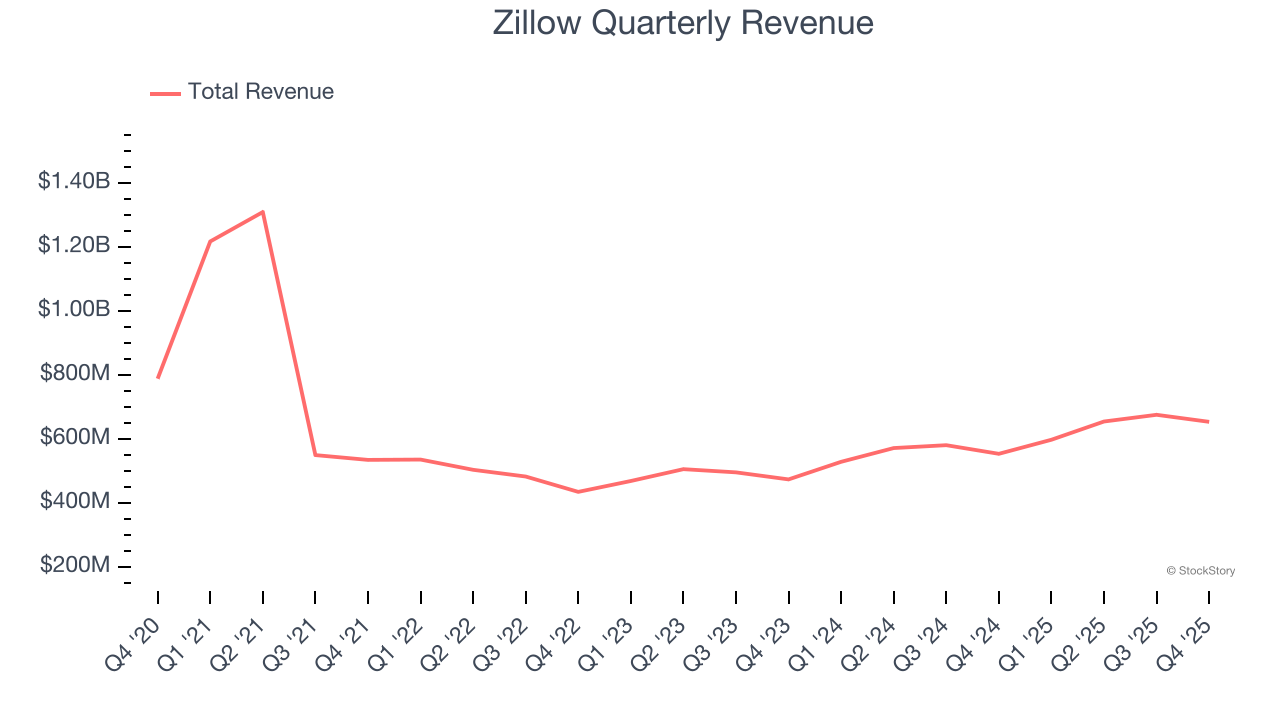

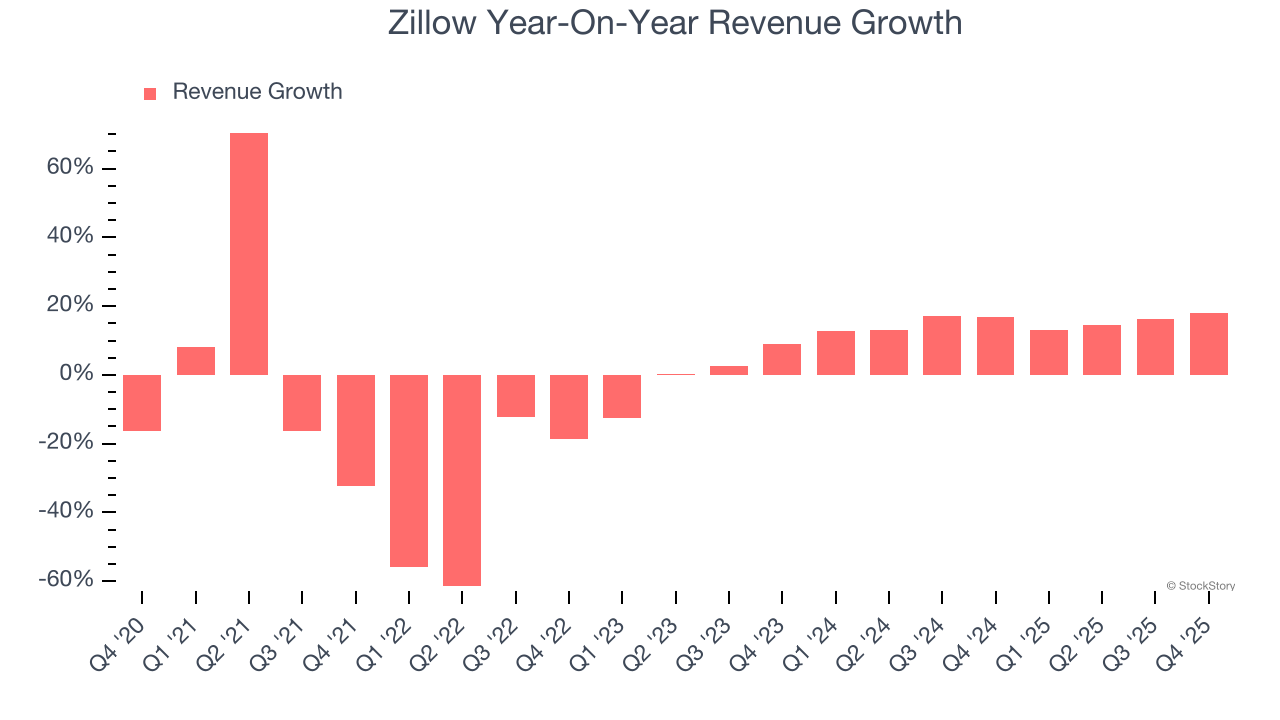

Online real estate marketplace Zillow (NASDAQ: ZG) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 18.1% year on year to $654 million. Its GAAP profit of $0.01 per share was $0.03 above analysts’ consensus estimates.

Is now the time to buy Zillow? Find out by accessing our full research report, it’s free.

Zillow (ZG) Q4 CY2025 Highlights:

- Revenue: $654 million vs analyst estimates of $650.5 million (18.1% year-on-year growth, 0.5% beat)

- EPS (GAAP): $0.01 vs analyst estimates of -$0.02 ($0.03 beat)

- Adjusted EBITDA: $149 million vs analyst estimates of $151.5 million (22.8% margin, 1.6% miss)

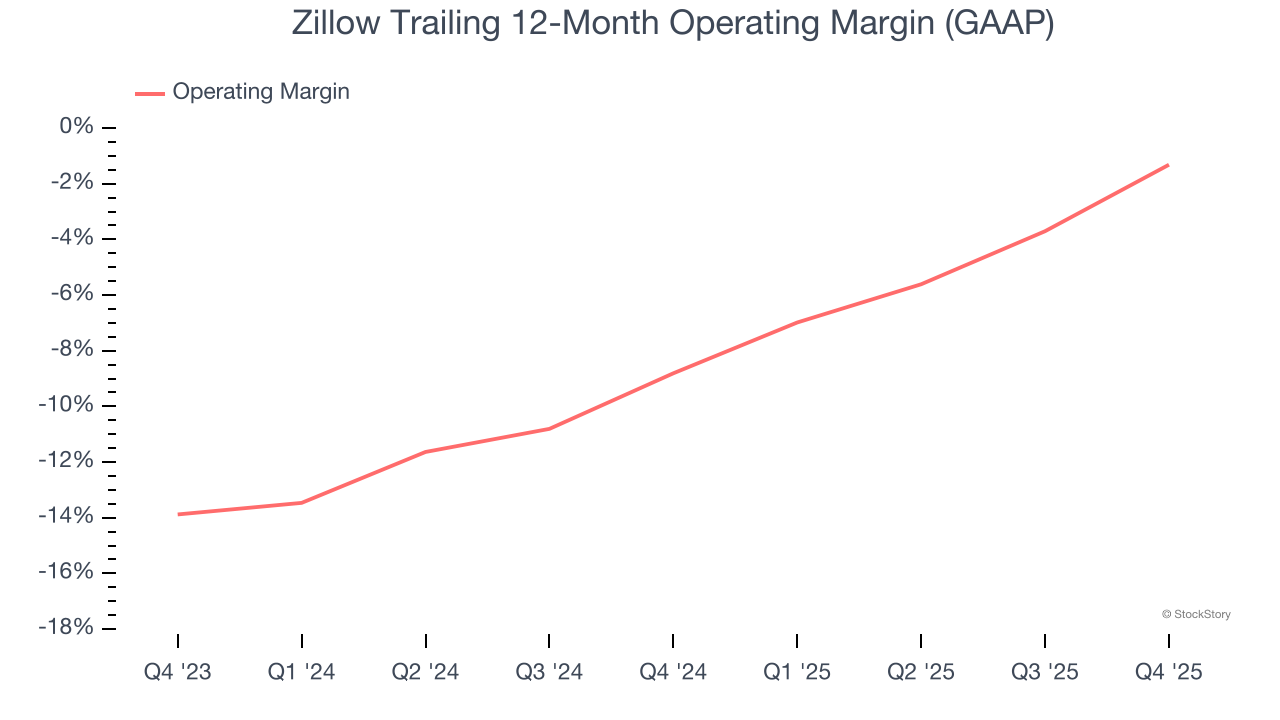

- Operating Margin: -1.7%, up from -12.5% in the same quarter last year

- Free Cash Flow Margin: 6.7%, down from 15.9% in the same quarter last year

- Market Capitalization: $13.12 billion

Company Overview

Founded by Expedia co-founders Lloyd Frink and Rich Barton, Zillow (NASDAQ: ZG) is the leading U.S. online real estate marketplace.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Zillow’s demand was weak over the last five years as its sales fell at a 5% annual rate. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Zillow’s annualized revenue growth of 15.2% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Zillow reported year-on-year revenue growth of 18.1%, and its $654 million of revenue exceeded Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 14.5% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and implies its newer products and services will help sustain its recent top-line performance.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Zillow’s operating margin has been trending up over the last 12 months, but it still averaged negative 4.8% over the last two years. This is due to its large expense base and inefficient cost structure.

In Q4, Zillow generated a negative 1.7% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

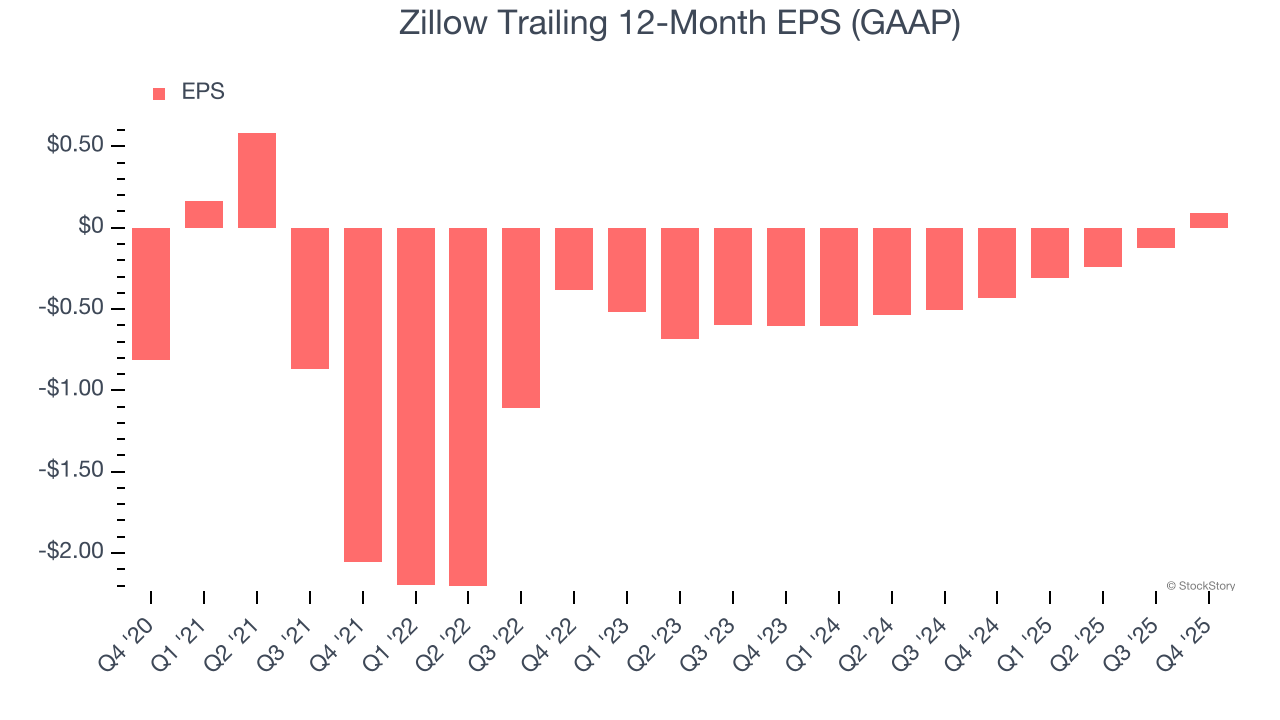

Zillow’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Zillow reported EPS of $0.01, up from negative $0.20 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Zillow’s full-year EPS of $0.09 to grow 527%.

Key Takeaways from Zillow’s Q4 Results

Revenue beat by a small amount, but adjusted EBITDA missed. Overall, this was a mixed quarter, and the stock traded down 5% to $51.68 immediately after reporting.

So do we think Zillow is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).