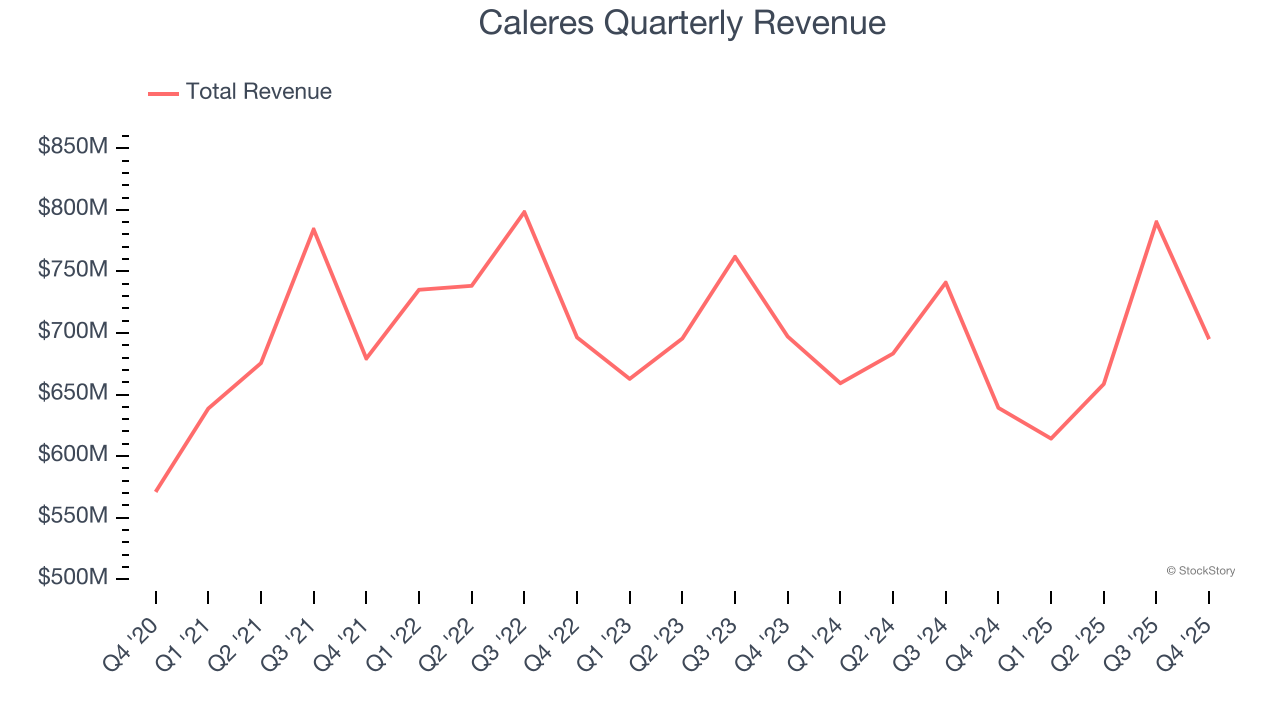

Footwear company Caleres (NYSE: CAL) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 8.7% year on year to $695.1 million. Its non-GAAP loss of $0.06 per share was 85.1% above analysts’ consensus estimates.

Is now the time to buy Caleres? Find out by accessing our full research report, it’s free.

Caleres (CAL) Q4 CY2025 Highlights:

- Revenue: $695.1 million vs analyst estimates of $685.4 million (8.7% year-on-year growth, 1.4% beat)

- Adjusted EPS: -$0.06 vs analyst estimates of -$0.40 (85.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.50 at the midpoint, missing analyst estimates by 0.9%

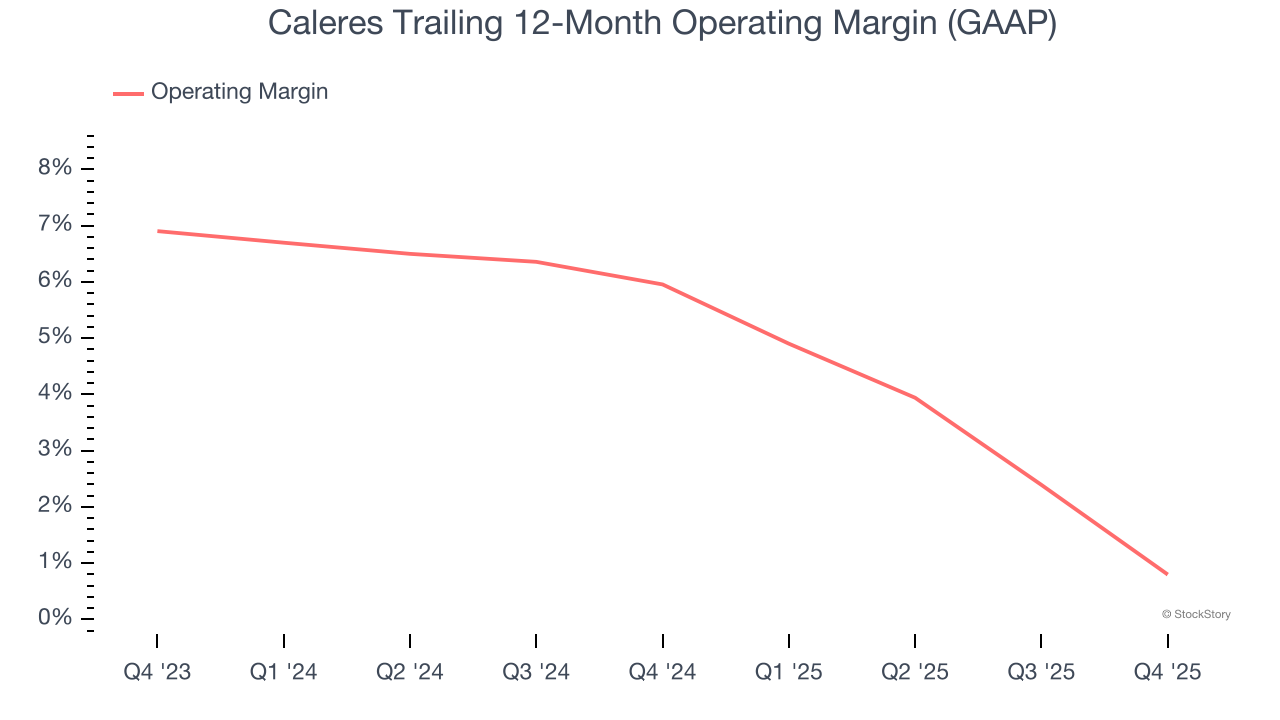

- Operating Margin: -3.8%, down from 2.5% in the same quarter last year

- Free Cash Flow Margin: 6.6%, up from 2.8% in the same quarter last year

- Market Capitalization: $300.3 million

“Caleres’ fourth quarter exceeded our earnings guidance with sales modestly above expectations and gross margin better than anticipated in both segments,” said Jay Schmidt, president and chief executive officer.

Company Overview

The owner of Dr. Scholl's, Caleres (NYSE: CAL) is a footwear company offering a range of styles.

Revenue Growth

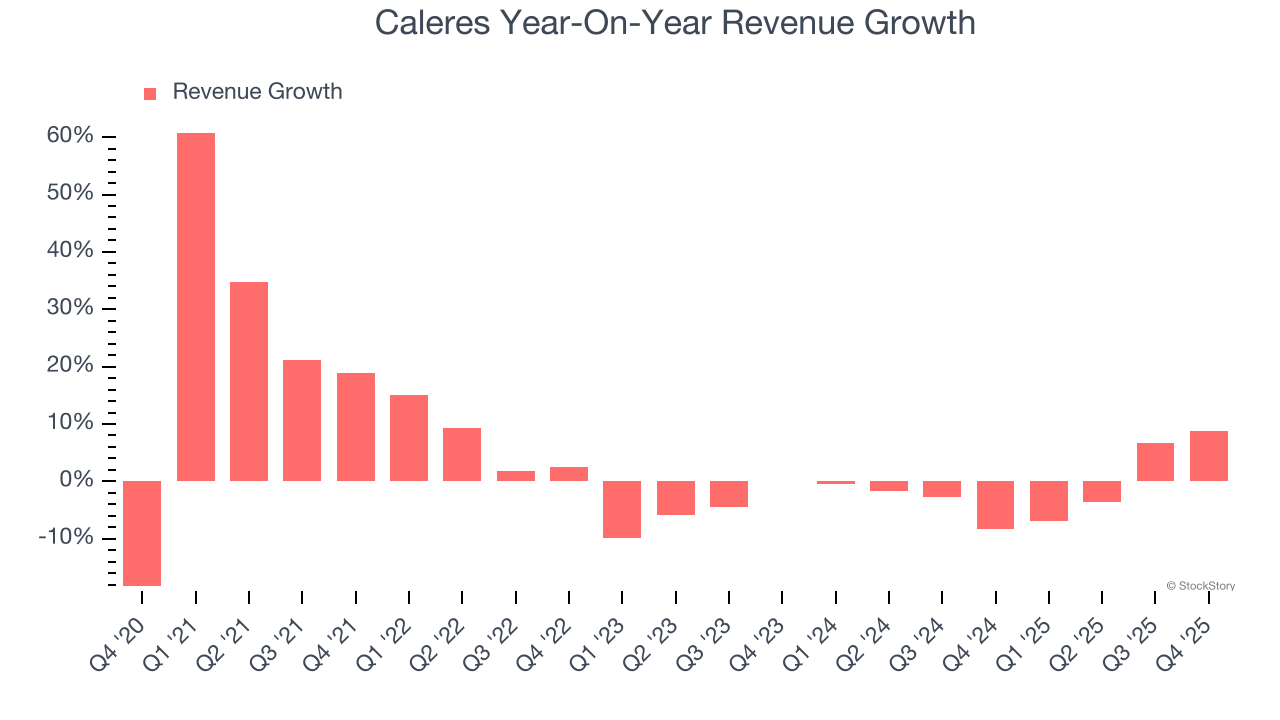

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Caleres’s sales grew at a weak 5.4% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Caleres’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.1% annually.

This quarter, Caleres reported year-on-year revenue growth of 8.7%, and its $695.1 million of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Caleres’s operating margin has shrunk over the last 12 months and averaged 3.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Caleres generated an operating margin profit margin of negative 3.8%, down 6.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

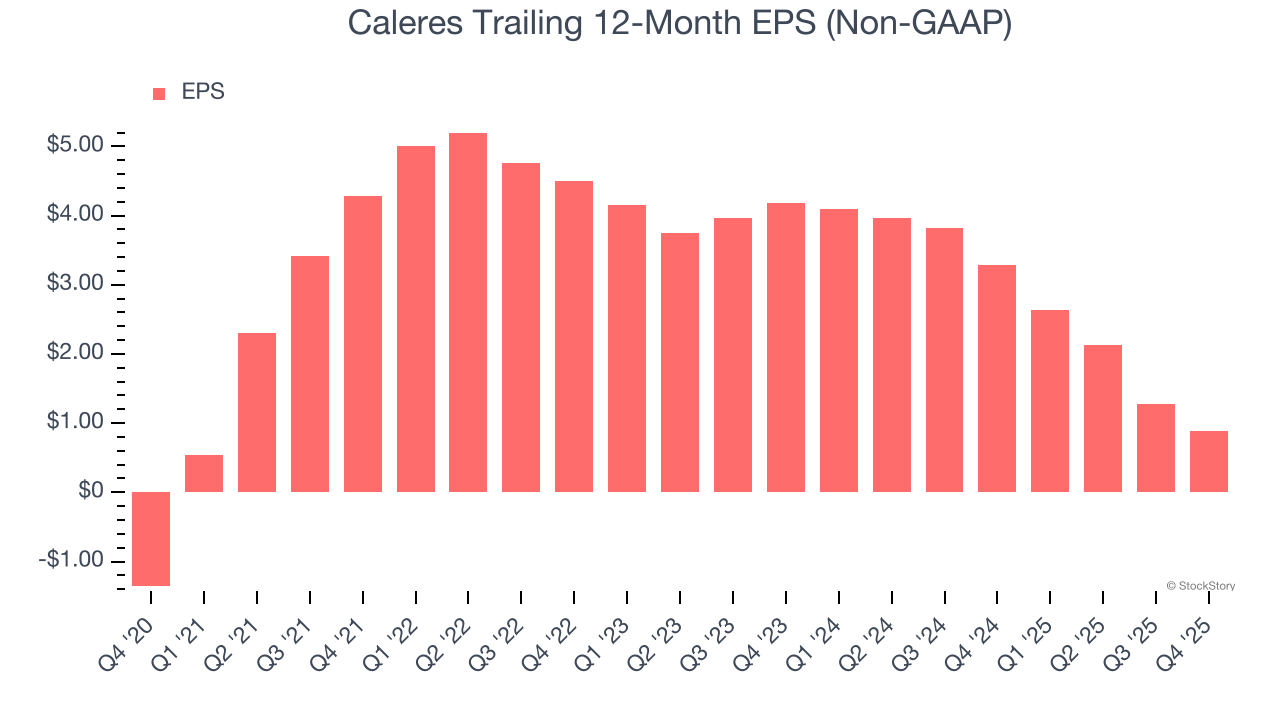

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Caleres’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Caleres reported adjusted EPS of negative $0.06, down from $0.33 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Caleres’s full-year EPS of $0.89 to grow 68.5%.

Key Takeaways from Caleres’s Q4 Results

It was good to see Caleres beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed. Overall, this print had some key positives. The stock traded up 9.5% to $9.66 immediately following the results.

Caleres put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).