Over the past six months, PennyMac Financial Services’s stock price fell to $94.66. Shareholders have lost 5% of their capital, which is disappointing considering the S&P 500 has climbed by 9.1%. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in PennyMac Financial Services, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is PennyMac Financial Services Not Exciting?

Even though the stock has become cheaper, we're swiping left on PennyMac Financial Services for now. Here are three reasons there are better opportunities than PFSI and a stock we'd rather own.

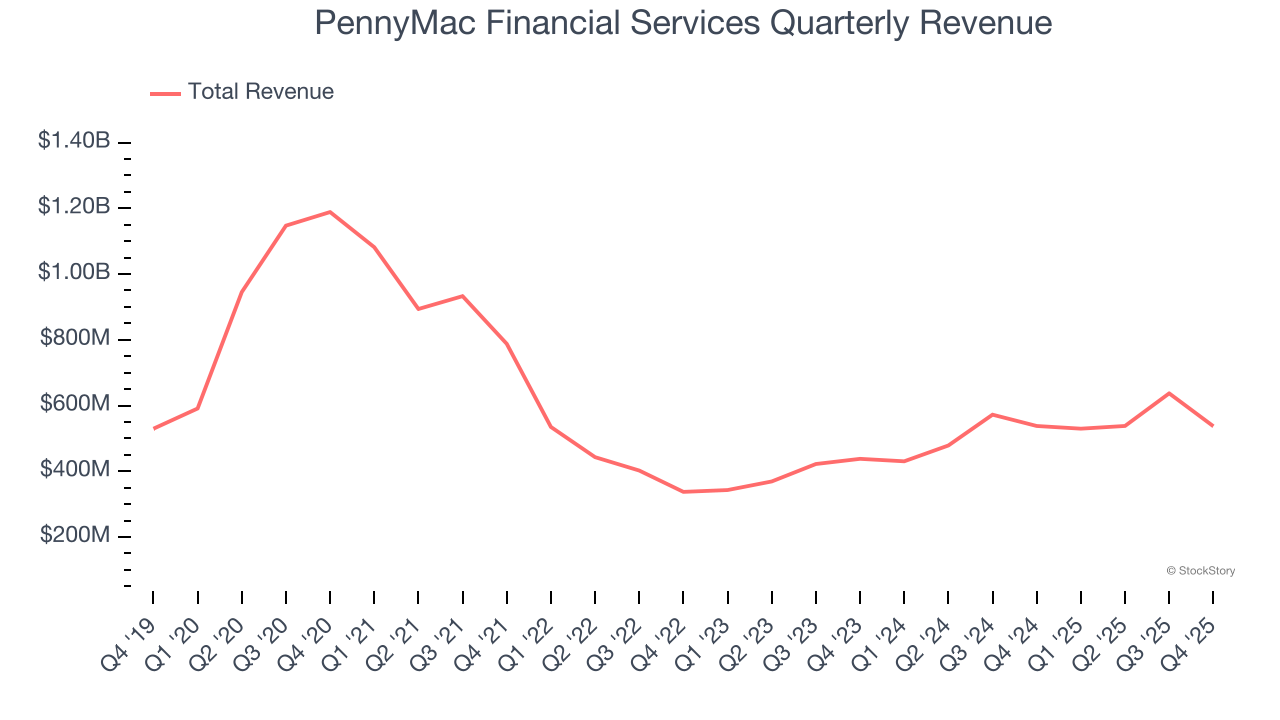

1. Revenue Spiraling Downwards

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

PennyMac Financial Services’s demand was weak over the last five years as its revenue fell at a 10.4% annual rate. This wasn’t a great result and is a sign of lacking business quality.

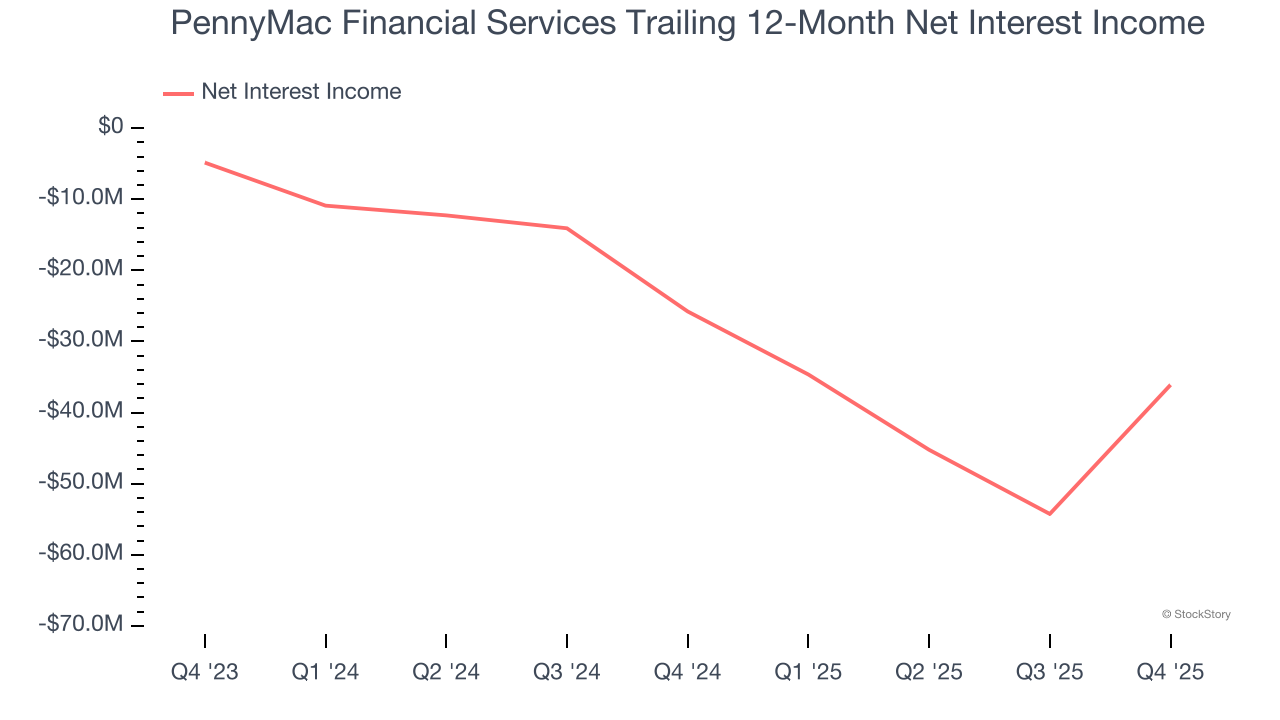

2. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

PennyMac Financial Services’s net interest income has grown at a 7.1% annualized rate over the last five years, worse than the broader banking industry.

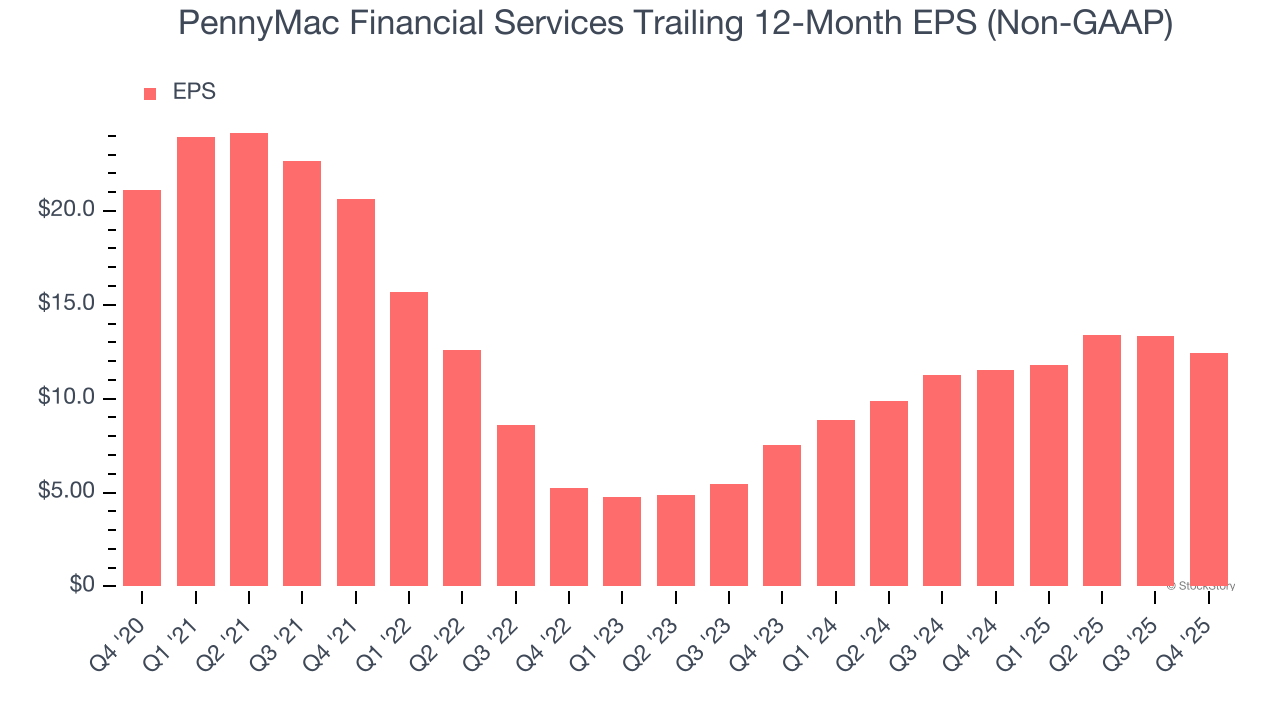

3. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for PennyMac Financial Services, its EPS and revenue declined by 10% and 10.4% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, PennyMac Financial Services’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

PennyMac Financial Services isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 1× forward P/B (or $94.66 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now. Let us point you toward the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.