Industrial materials and tools company Kennametal (NYSE: KMT) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 2.7% year on year to $482.1 million. Next quarter’s revenue guidance of $490 million underwhelmed, coming in 5.4% below analysts’ estimates. Its non-GAAP profit of $0.25 per share was in line with analysts’ consensus estimates.

Is now the time to buy Kennametal? Find out by accessing our full research report, it’s free.

Kennametal (KMT) Q4 CY2024 Highlights:

- Revenue: $482.1 million vs analyst estimates of $487 million (2.7% year-on-year decline, 1% miss)

- Adjusted EPS: $0.25 vs analyst estimates of $0.26 (in line)

- The company dropped its revenue guidance for the full year to $1.98 billion at the midpoint from $2.05 billion, a 3.7% decrease

- Management lowered its full-year Adjusted EPS guidance to $1.18 at the midpoint, a 21.7% decrease

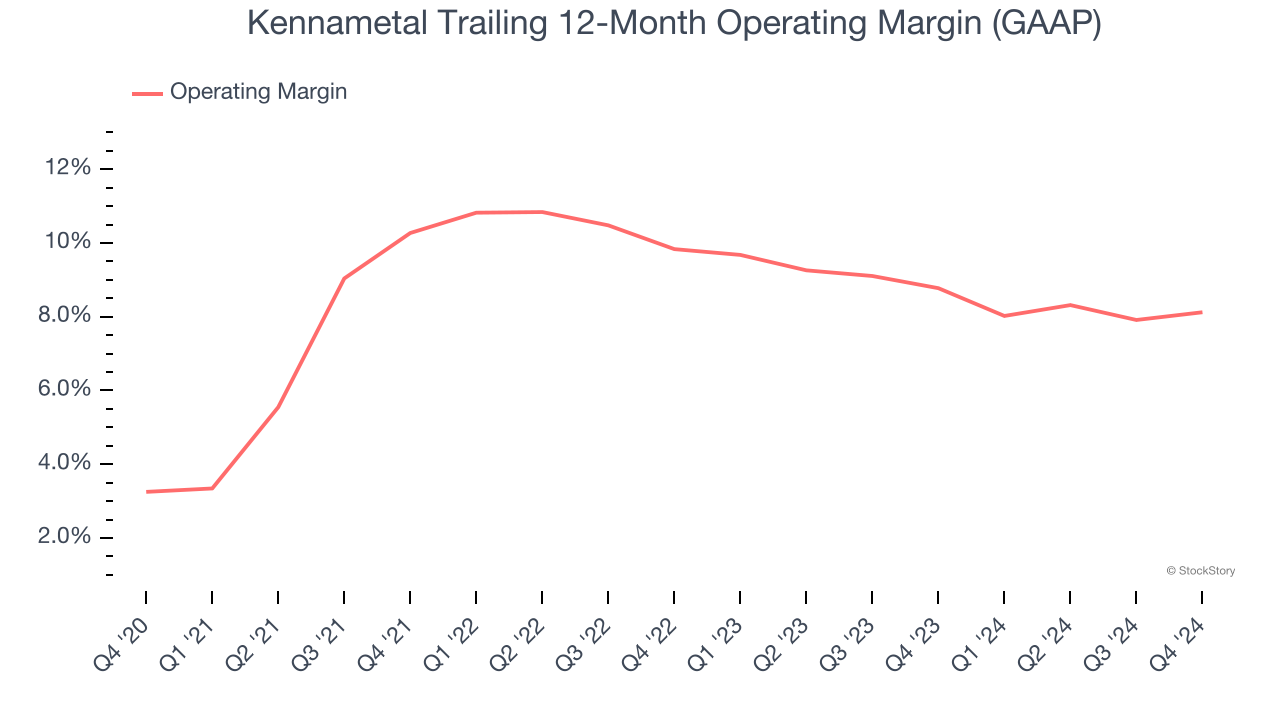

- Operating Margin: 6.6%, in line with the same quarter last year

- Free Cash Flow Margin: 7.4%, similar to the same quarter last year

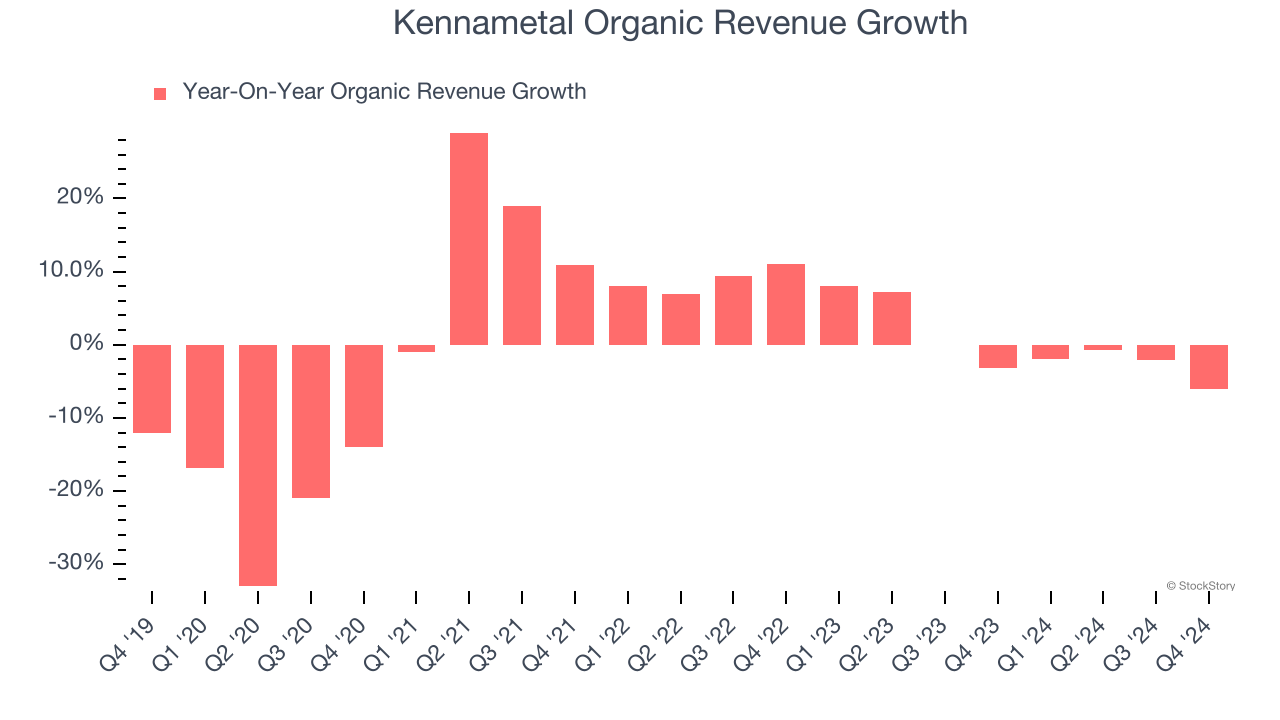

- Organic Revenue fell 6% year on year (-3.2% in the same quarter last year)

- Market Capitalization: $1.82 billion

"This quarter we once again generated strong cash flow from operations," said Sanjay Chowbey, President and CEO.

Company Overview

Involved in manufacturing hard tips of anti-tank projectiles in World War II, Kennametal (NYSE: KMT) is a provider of industrial materials and tools for various sectors.

Professional Tools and Equipment

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

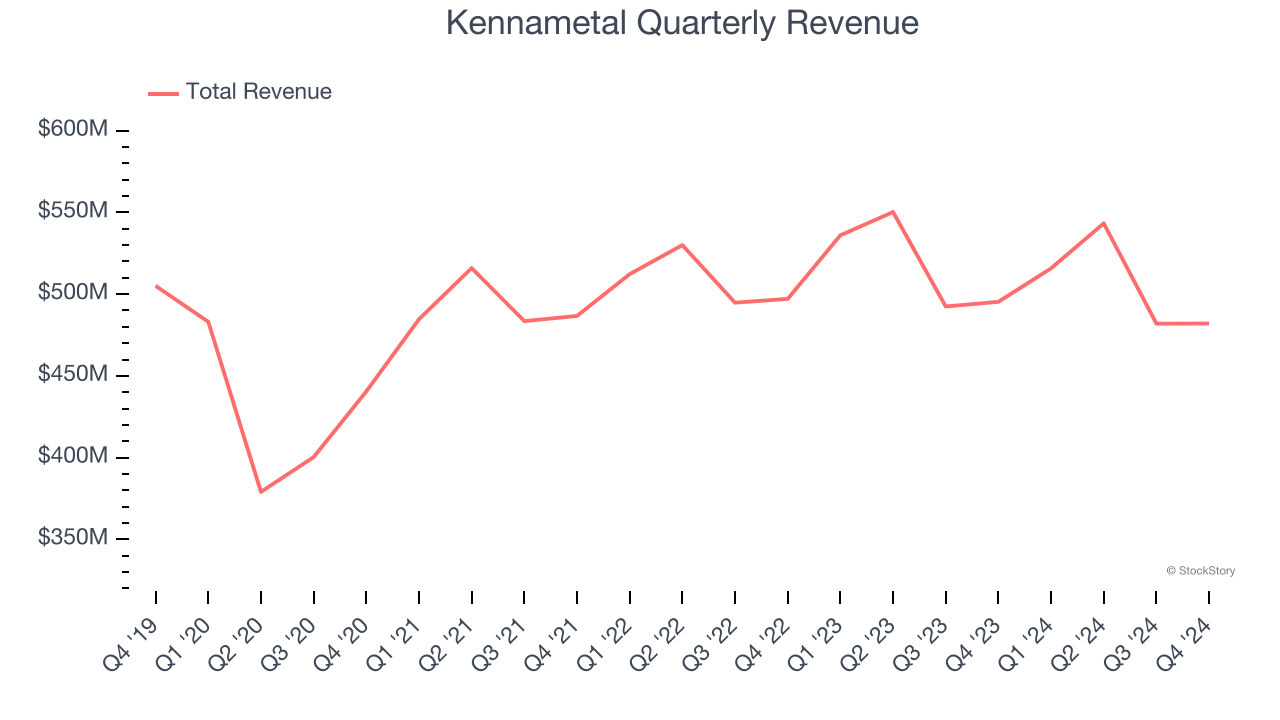

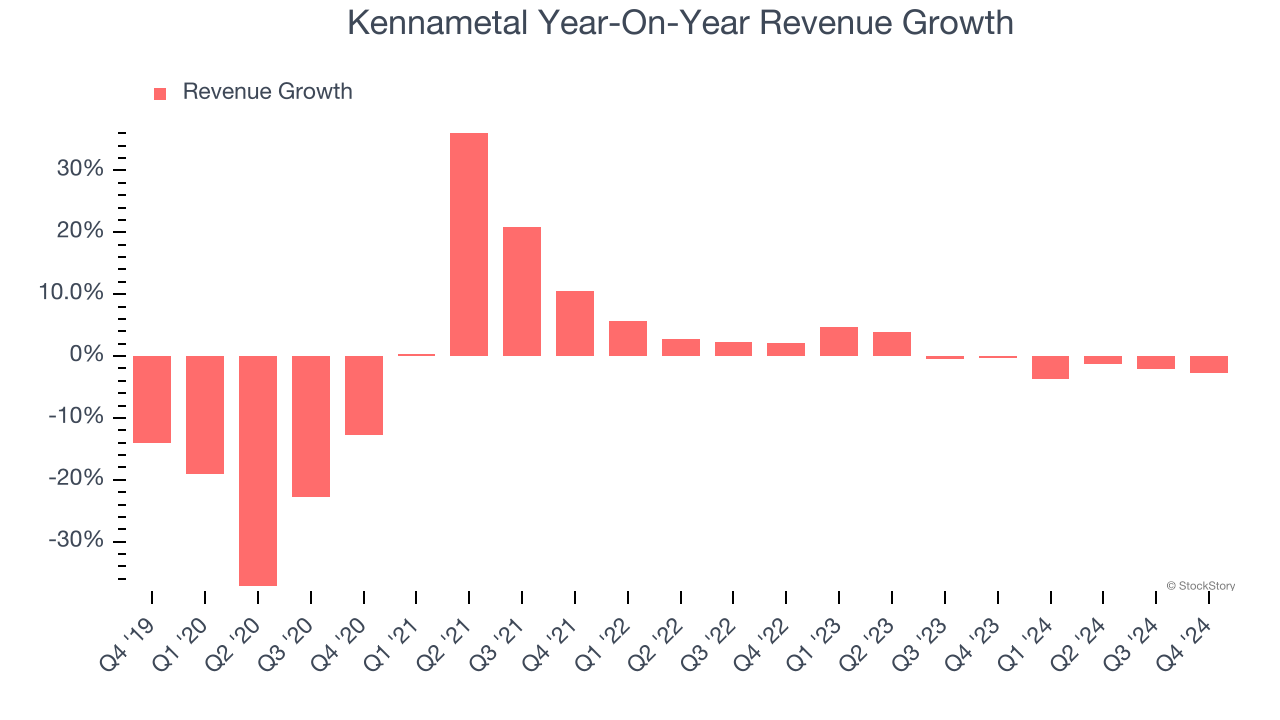

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Kennametal struggled to consistently generate demand over the last five years as its sales dropped at a 1.9% annual rate. This fell short of our benchmarks and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Kennametal’s revenue over the last two years was flat, sugggesting its demand was weak but stabilized after its initial drop in sales.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Kennametal’s organic revenue was flat. Because this number aligns with its normal revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Kennametal missed Wall Street’s estimates and reported a rather uninspiring 2.7% year-on-year revenue decline, generating $482.1 million of revenue. Company management is currently guiding for a 5% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2% over the next 12 months. Although this projection suggests its newer products and services will catalyze better top-line performance, it is still below the sector average.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Kennametal has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 8.2%, higher than the broader industrials sector.

Looking at the trend in its profitability, Kennametal’s operating margin rose by 4.9 percentage points over the last five years, showing its efficiency has improved.

This quarter, Kennametal generated an operating profit margin of 6.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

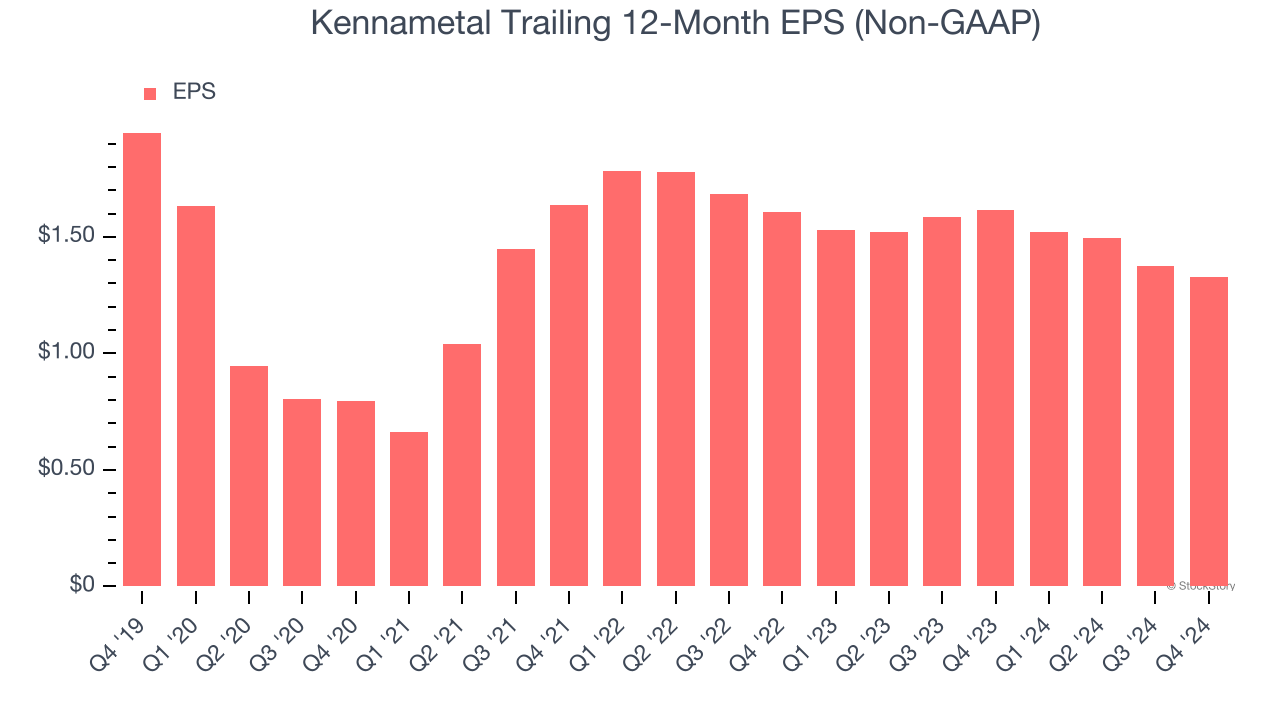

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Kennametal, its EPS declined by more than its revenue over the last five years, dropping 7.4% annually. However, its operating margin actually expanded during this time and it repurchased its shares, telling us the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Kennametal, its two-year annual EPS declines of 9.1% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Kennametal reported EPS at $0.25, down from $0.30 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Kennametal’s full-year EPS of $1.33 to grow 15.2%.

Key Takeaways from Kennametal’s Q4 Results

We struggled to find many positives in these results. Its full-year EPS guidance missed significantly and its revenue guidance for next quarter also fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4% to $22.51 immediately following the results.

The latest quarter from Kennametal’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.