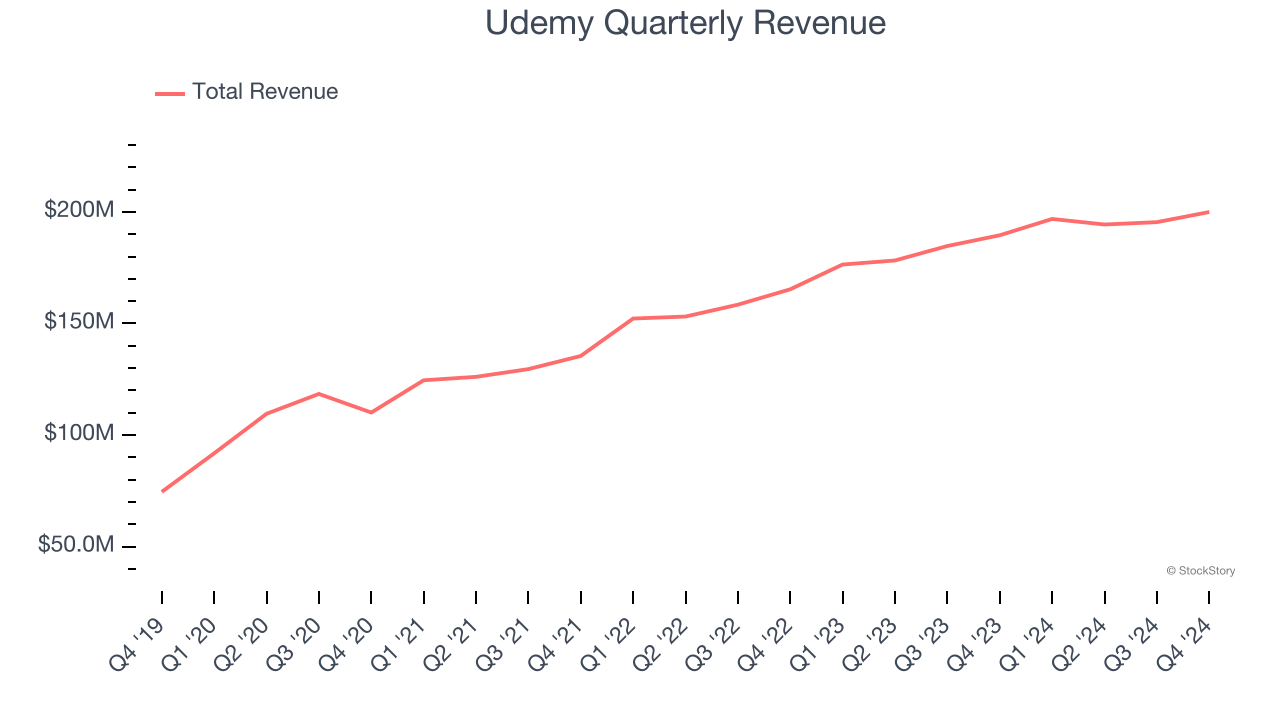

Online learning platform Udemy (NASDAQ: UDMY) reported revenue ahead of Wall Street’s expectations in Q4 CY2024, with sales up 5.5% year on year to $199.9 million. On the other hand, next quarter’s revenue guidance of $197 million was less impressive, coming in 2.7% below analysts’ estimates. Its non-GAAP profit of $0.10 per share was 53.4% above analysts’ consensus estimates.

Is now the time to buy Udemy? Find out by accessing our full research report, it’s free.

Udemy (UDMY) Q4 CY2024 Highlights:

- Revenue: $199.9 million vs analyst estimates of $194.7 million (5.5% year-on-year growth, 2.7% beat)

- Adjusted EPS: $0.10 vs analyst estimates of $0.07 (53.4% beat)

- Adjusted EBITDA: $19.48 million vs analyst estimates of $11.78 million (9.7% margin, 65.4% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $795 million at the midpoint, missing analyst estimates by 1.5% and implying 1.1% growth (vs 8% in FY2024)

- EBITDA guidance for the upcoming financial year 2025 is $80 million at the midpoint, above analyst estimates of $70.08 million

- Monthly Active Buyers: 1.32 million, up 1.3 million year on year

- Market Capitalization: $1.13 billion

Company Overview

With courses ranging from investing to cooking to computer programming, Udemy (NASDAQ: UDMY) is an online learning platform that connects learners with expert instructors who specialize in a wide range of topics.

Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Udemy grew its sales at a solid 15.1% compounded annual growth rate. Its growth beat the average consumer internet company and shows its offerings resonate with customers.

This quarter, Udemy reported year-on-year revenue growth of 5.5%, and its $199.9 million of revenue exceeded Wall Street’s estimates by 2.7%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.6% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Key Takeaways from Udemy’s Q4 Results

We were impressed by Udemy’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year revenue guidance missed significantly and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, we think this was still a decent quarter with some key metrics above expectations. The stock traded up 6.9% to $8.36 immediately after reporting.

Indeed, Udemy had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.