Dollar Tree’s 32.6% return over the past six months has outpaced the S&P 500 by 19.5%, and its stock price has climbed to $131.25 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Dollar Tree, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Is Dollar Tree Not Exciting?

We’re happy investors have made money, but we're sitting this one out for now. Here are three reasons there are better opportunities than DLTR and a stock we'd rather own.

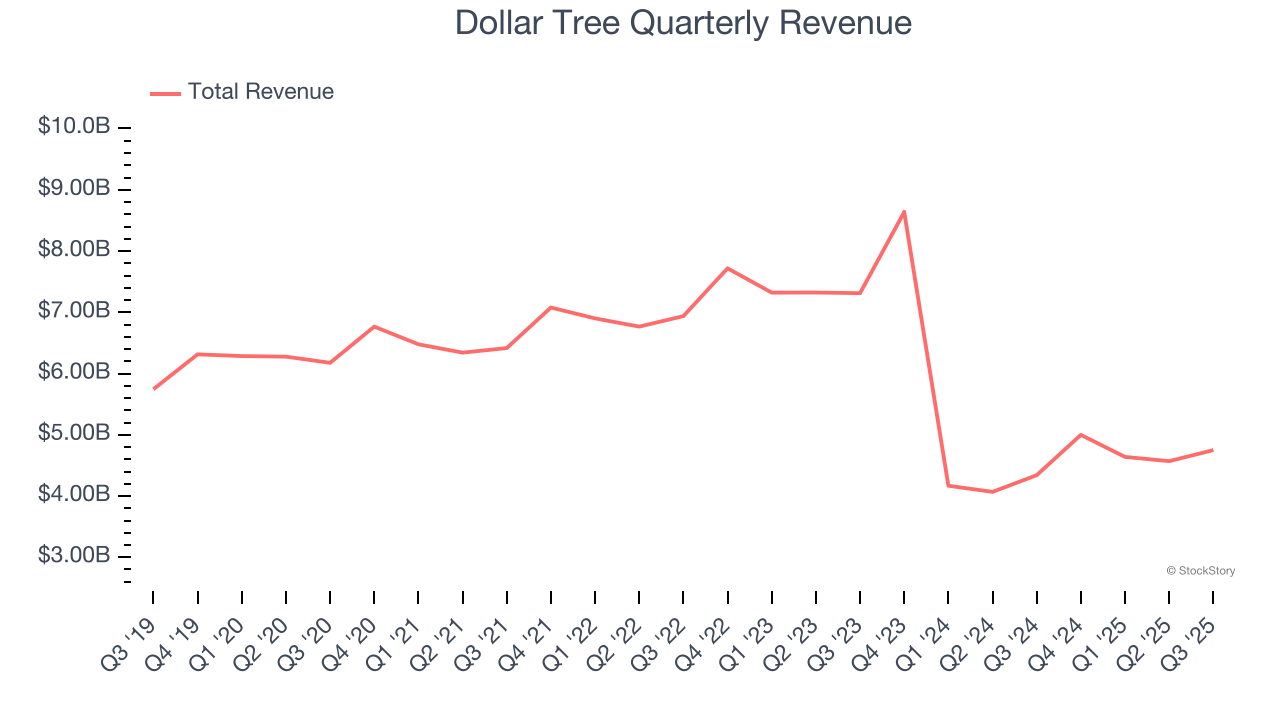

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Dollar Tree struggled to consistently generate demand over the last three years as its sales dropped at a 11.9% annual rate. This was below our standards and signals it’s a lower quality business.

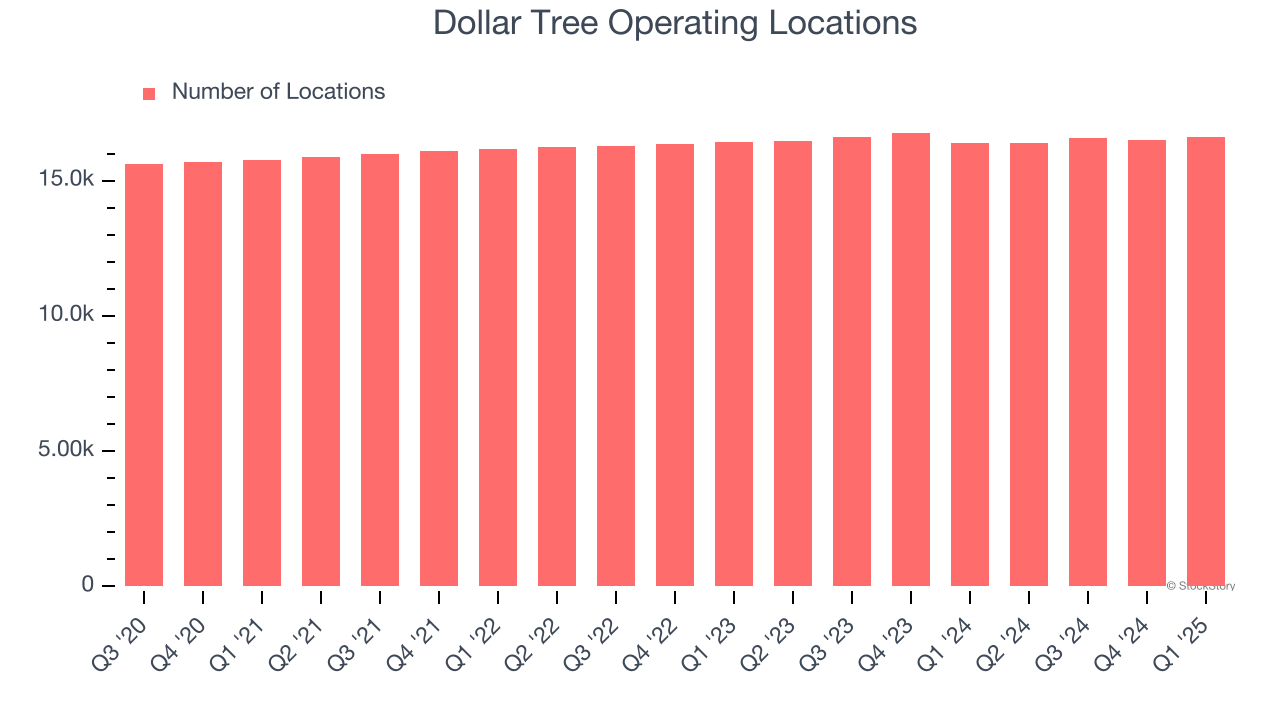

2. Lack of New Stores, a Headwind for Revenue

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Over the last two years, Dollar Tree has kept its store count flat while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Dollar Tree reports its store count intermittently, so some data points are missing in the chart below.

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Dollar Tree historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 9.7%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

Final Judgment

Dollar Tree’s business quality ultimately falls short of our standards. With its shares outperforming the market lately, the stock trades at 20.4× forward P/E (or $131.25 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.