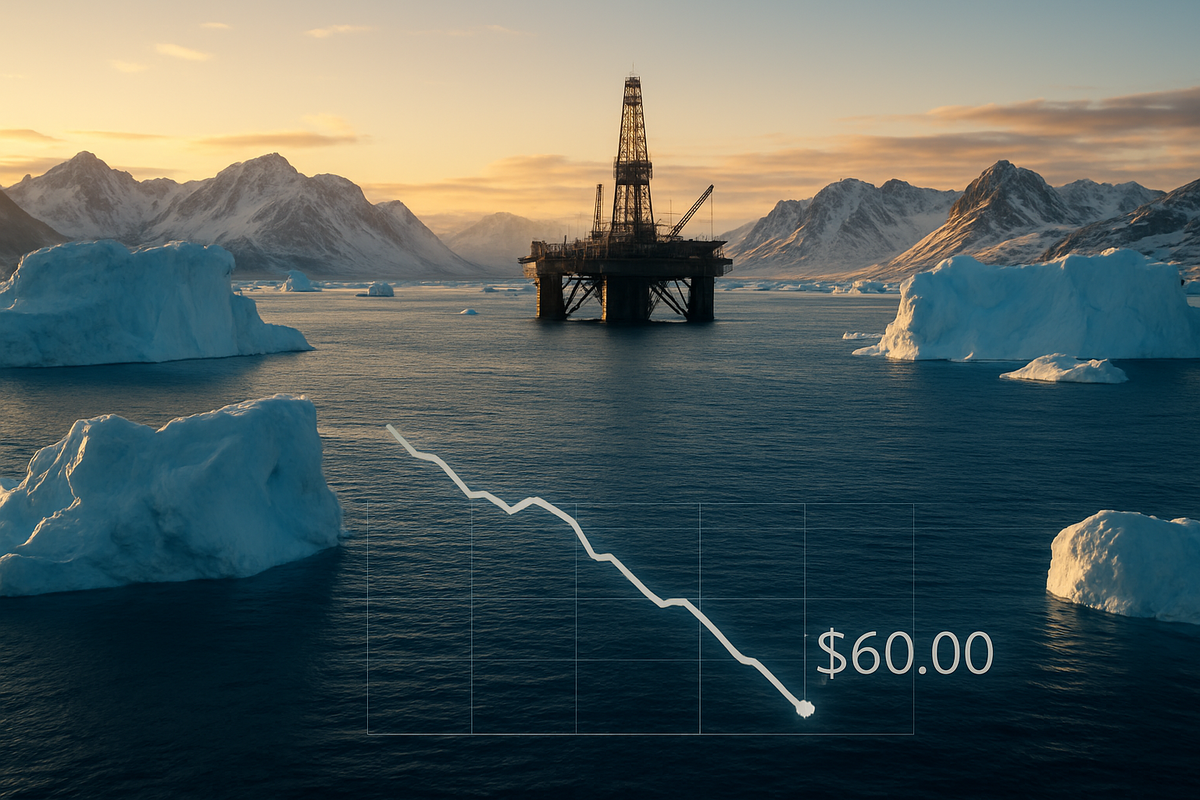

Energy markets witnessed a significant shift this week as West Texas Intermediate (WTI) crude oil futures tumbled toward the $60 per barrel mark, a level not seen with such stability since the previous year. The decline, which saw WTI trading near $60.37 and Brent Crude hovering around $64, marks a sharp reversal from the volatility that characterized the start of the 2026 trading year. This downward trajectory is primarily attributed to a dual-pronged pressure of easing geopolitical tensions in the Arctic and a surprising surge in domestic crude inventories.

The cooling of prices follows a pivotal moment in international diplomacy where President Trump effectively ruled out the use of military force or aggressive coercion regarding the United States' long-standing interest in Greenland. This declaration, coupled with data from the Energy Information Administration (EIA) showing a substantial build in U.S. oil stockpiles, has stripped away the "geopolitical risk premium" that had artificially inflated prices throughout the early weeks of January.

The dramatic slide in oil prices found its catalyst in the Swiss Alps during the World Economic Forum in Davos. On January 21, 2026, following high-level discussions with NATO Secretary-General Mark Rutte and Danish officials, the Trump administration signaled a shift from aggressive rhetoric to a "commercial and cooperative" framework for the Arctic. By ruling out the use of force and withdrawing the threat of 10%–25% tariffs on Denmark, the administration effectively defused a brewing diplomatic crisis over Greenland’s strategic minerals and territory. Markets immediately responded, with WTI dropping nearly 5% within 48 hours as the specter of a disrupted Northern Sea Route faded.

Simultaneously, the domestic supply picture provided the fundamental "gravity" for this price drop. The latest EIA report revealed that commercial crude inventories rose by approximately 3.4 million barrels in mid-January, significantly defying analyst expectations of a seasonal draw. This inventory build is a testament to the relentless efficiency of the U.S. shale patch, which reached a record production high of 13.6 million barrels per day (b/d) in late 2025. With tanks filling up and the threat of conflict receding, the market's previous bullish momentum has been thoroughly extinguished.

The timeline of this slump began in early January when WTI spiked briefly on news of the "Arctic Sentry" operations, a move by NATO to counter Russian influence that many feared would lead to a direct confrontation. However, the subsequent "Davos De-escalation" served as a cooling agent. Investors who had hedged against a possible Arctic conflict were forced to liquidate positions, leading to the rapid price correction observed today, January 23, 2026.

The shift to $60 oil creates a clear divide between winners and losers across the S&P 500. The most immediate beneficiaries are the major domestic carriers, such as United Airlines (NASDAQ: UAL) and Delta Air Lines (NYSE: DAL). For these companies, fuel typically represents 20% to 30% of operating expenses. United Airlines, which recently reported record Q4 revenue of $15.4 billion, stands to see its margins expand even further if jet fuel prices track the decline in crude. Analysts suggest that the airline industry could be headed for a record-breaking 2026 as lower input costs collide with resilient consumer demand for premium travel.

Conversely, the "Big Oil" giants face a more complex environment. ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have enjoyed a period of high profitability, but a sustained period of $60 oil will test their capital discipline. While ExxonMobil’s integrated model provides a natural hedge through its refining arm—which benefits from lower feedstock costs—its upstream exploration margins will narrow. Chevron, however, may find a unique silver lining; the administration’s "Venezuelan Oil Reset" policy could allow Chevron to leverage its existing infrastructure in South America to offset lower prices with higher volume, provided the political landscape remains stable.

The renewable energy sector and electric vehicle manufacturers like Tesla (NASDAQ: TSLA) may face headwinds from cheaper fossil fuels. When gasoline prices at the pump decline, the economic incentive for consumers to switch to electric vehicles often softens. However, many analysts argue that the structural shift toward electrification is now sufficiently decoupled from short-term oil volatility, though TSLA’s near-term growth projections may see slight adjustments if $60 oil becomes the new semi-permanent floor.

This event fits into a broader 2026 trend of "market normalization" following years of post-pandemic and regional conflict volatility. The easing of the Greenland risk premium highlights a growing trend where economic statecraft—specifically the use of tariffs and investment frameworks—is replacing traditional military posturing as the primary mover of commodity markets. The "Tariffs over Tomahawks" strategy has proven to be a potent tool for the current administration, allowing for geopolitical maneuvering without the catastrophic supply disruptions associated with 20th-century warfare.

Furthermore, the record U.S. production levels signal a permanent shift in the global energy hierarchy. The U.S. has effectively become the world’s "swing producer," a role traditionally held by the OPEC+ bloc. By maintaining production at 13.6 million b/d, the U.S. has created a supply cushion that makes it difficult for geopolitical shocks to sustain high prices for long. This abundance has significant regulatory implications, as the focus in Washington may shift from encouraging production to managing the infrastructure required to export this surplus to energy-hungry markets in Asia and Europe.

Historically, this moment draws comparisons to the mid-2010s oil glut, where U.S. shale efficiency outpaced global demand growth. The difference today is the sophistication of the risk management. In 2026, the market is not just dealing with "too much oil," but with a "calmer world" where the primary threats to supply—Arctic sovereignty and South American instability—are being managed through diplomatic "resets" rather than protracted stalemates.

In the short term, market participants should expect WTI to consolidate around the $58–$62 range. The "Greenland Deal" is still in its framework stage, and any friction in the final negotiations between Washington, Copenhagen, and Nuuk could reintroduce minor volatility. However, the long-term outlook remains bearish for prices. The EIA’s forecast of WTI averaging $52 per barrel for the full year of 2026 appears increasingly plausible if global demand growth continues to lag behind the 2.1 million b/d production surge expected this year.

Energy companies will likely pivot toward "efficiency-first" strategies. We may see a slowdown in new offshore exploration projects in favor of optimizing existing shale wells in the Permian Basin. For investors, the challenge will be identifying which companies can remain cash-flow positive at $55–$60 oil. This environment favors low-cost producers and integrated majors with strong balance sheets. Strategic adaptations may also include a renewed focus on carbon capture and storage (CCS) as a way to maintain regulatory favor in an era of fossil fuel abundance.

The retreat of WTI crude to the $60 level is more than just a fluctuation in a ticker symbol; it is a reflection of a changing world order where the U.S. is using its energy and economic dominance to settle long-standing geopolitical disputes. The "Greenland risk premium" served as a reminder of how sensitive markets are to the rhetoric of world leaders, but the current slump proves that fundamentals—namely record-breaking U.S. production and rising stockpiles—eventually win the day.

Investors should move forward with a focus on high-quality equities in the transportation and industrial sectors that stand to gain from lower energy costs. While the oil majors remain essential components of the energy landscape, their growth will likely be driven by volume and refining efficiency rather than price spikes. In the coming months, the key indicators to watch will be the finalization of the Arctic framework and the weekly EIA inventory reports, which will signal whether the current stockpile build is a seasonal anomaly or a permanent feature of the 2026 economy.

This content is intended for informational purposes only and is not financial advice.