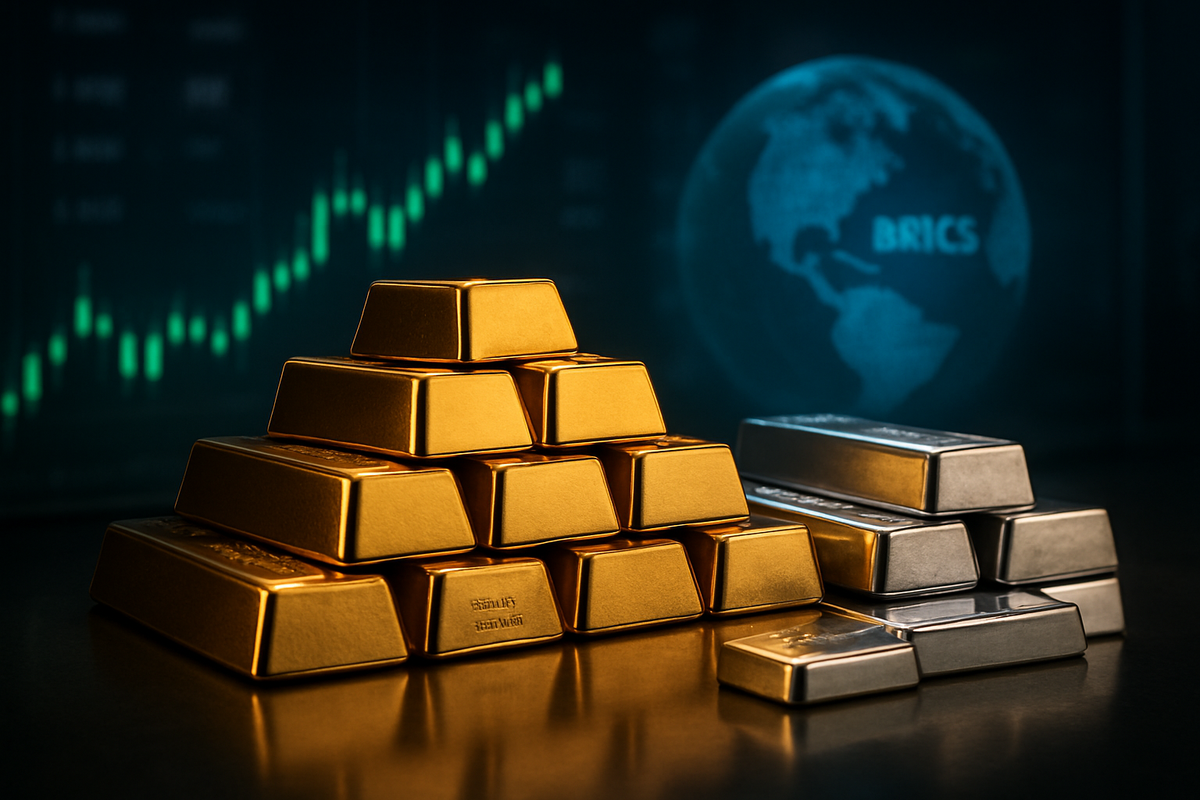

As the world celebrates the 2025 holiday season, the financial markets are witnessing a historic milestone that has fundamentally recalibrated the global economy. In a year defined by the "Hard Asset Super-Cycle," gold has officially breached the psychological $4,500 per ounce barrier, while silver has staged a vertical ascent to surpass $72 per ounce. This unprecedented rally marks a 70% annual gain for gold and a staggering 140% surge for silver, cementing 2025 as the most transformative year for precious metals in nearly half a century.

The immediate implications of this surge are profound, signaling a massive shift in investor sentiment away from traditional fiat-denominated assets and toward tangible stores of value. With the U.S. dollar experiencing its steepest annual decline in a decade and central banks across the globe—particularly within the BRICS bloc—abandoning sovereign debt in favor of physical bullion, the "Golden Christmas" of 2025 represents more than just a price spike; it is a structural realignment of the international monetary system.

A Year of Vertical Ascent: The Path to $4,500

The rally that culminated in this week’s record highs began in earnest during the first quarter of 2025, following a decisive pivot by the Federal Reserve. After a period of "higher for longer" interest rates, the Fed implemented three separate rate cuts throughout 2025, totaling 75 basis points. These cuts lowered the opportunity cost of holding non-yielding assets, providing the initial spark for the gold market. By mid-summer, as the U.S. Dollar Index (DXY) tumbled by nearly 10%, the spark turned into a wildfire.

The timeline of the surge was punctuated by a "physical squeeze" in the silver market during the third quarter. Unlike gold, which serves primarily as a monetary hedge, silver’s dual role as an industrial metal became the primary driver of its 140% gain. Massive demand from the artificial intelligence (AI) infrastructure boom and the continued expansion of green energy sectors led to a severe supply deficit. By the time the market reached December, spot silver hit a peak of $72.70, a level many analysts had deemed impossible just twelve months prior.

Key stakeholders in this rally extend beyond retail investors to the highest levels of statecraft. The primary catalysts were the BRICS nations (Brazil, Russia, India, China, and South Africa), who collectively purchased a record 850 tons of gold in 2025. This aggressive accumulation was not merely a hedge against inflation but a coordinated effort to insulate their economies from Western sanctions and the volatility of the dollar. The rally reached its fever pitch in late 2025 with the launch of "The Unit," a gold-backed settlement currency used by the BRICS bloc, which provided a new, high-volume utility for physical gold in international trade.

Winners and Losers in the Great Metal Rush

The primary beneficiaries of this price explosion have been the mining companies and streaming firms that provide the world’s supply. Coeur Mining (NYSE: CDE) emerged as the standout performer of the year, posting a 229% year-to-date return as its Rochester facility expansion perfectly timed the silver squeeze. Similarly, Pan American Silver Corp. (NYSE: PAAS) and First Majestic Silver Corp. (NYSE: AG) saw their profit margins expand exponentially, as the cost of extraction remained relatively stable while the sale price of their product more than doubled.

The industry’s "streaming" giants have also thrived. Wheaton Precious Metals Corp. (NYSE: WPM) captured the upside of $72 silver and $4,500 gold without the direct operational risks or inflationary pressures associated with running a mine. Even the diversified giants, Newmont Corporation (NYSE: NEM) and Barrick Gold Corporation (NYSE: GOLD), saw their market caps swell by hundreds of billions of dollars, though they were slightly outperformed by the more agile, silver-focused miners. Investors also flooded into exchange-traded funds, with the iShares Silver Trust (NYSE: SLV) and the SPDR Gold Shares (NYSE: GLD) seeing record-breaking inflows as "paper" gold and silver markets struggled to keep pace with physical demand.

However, the rally has not been without its casualties. Industrial users of silver, particularly in the solar energy and electronics sectors, have faced a "cost-push" crisis. Companies involved in the manufacturing of photovoltaic cells have seen their input costs skyrocket, leading to a slowdown in project deployments and a scramble for silver alternatives. Furthermore, traditional jewelry retailers have been forced to hike prices to levels that have effectively priced out the middle-class consumer, leading to a sharp decline in discretionary jewelry sales during the 2025 holiday season.

De-Dollarization and the New Monetary Order

The wider significance of the 2025 rally lies in its role as a catalyst for de-dollarization. The purchase of 850 tons of gold by BRICS nations represents a historic shift in central bank reserves. For decades, the U.S. Treasury was the undisputed "risk-free" asset of choice; in 2025, that title shifted toward physical bullion. The repatriation of 100 tons of gold by India from the United Kingdom earlier this year served as a harbinger of this trend, signaling a growing distrust in Western financial custody.

Historically, this event draws comparisons to the late 1970s, when stagflation drove gold to then-record highs. However, the 2025 rally is distinct because it is driven by technological demand (AI and Green Tech) as much as it is by monetary policy. The introduction of "The Unit" currency—pegged 40% to gold—marks the first time since the collapse of Bretton Woods that gold has been officially reintegrated into a major international trading framework. This move has created a "floor" for gold prices that many analysts believe will prevent a return to the sub-$3,000 levels of the early 2020s.

The ripple effects are being felt in the geopolitical arena as well. The weakening of the dollar has reduced the efficacy of U.S. financial sanctions, as more nations move their trade settlements into gold-backed or local-currency systems. This shift has prompted urgent discussions in Washington regarding the future of the dollar's reserve status and the potential need for a Central Bank Digital Currency (CBDC) that could compete with the rising "hard asset" alternatives.

The Road Ahead: Will the Momentum Hold?

Looking toward 2026, the market is divided on whether these prices are sustainable. In the short term, a technical correction is likely, as traders who entered positions early in 2025 look to lock in their historic profits. However, the structural supply deficits in the silver market suggest that any dip in silver prices may be short-lived. Analysts are already projecting that if industrial demand from the AI sector continues its current trajectory, silver could challenge $80 to $90 per ounce by late next year.

For gold, the long-term outlook remains tethered to the BRICS nations' continued adoption of "The Unit." If more countries join the bloc and adopt the gold-backed settlement system, the demand for physical reserves will remain insatiable. Some aggressive forecasts suggest gold could challenge the $5,000 mark by the end of 2026, especially if the Federal Reserve is forced to continue rate cuts to support a cooling U.S. labor market. The primary challenge for the market will be the potential for "regulatory headwinds," as governments may seek to tax "windfall profits" from mining companies or implement new reporting requirements for physical gold holdings.

Final Thoughts: A New Normal for Investors

The historic rally of 2025 has fundamentally changed the definition of a "balanced portfolio." The days of gold and silver being viewed as "pet rocks" or "relics of the past" are over. In a world of high debt, currency debasement, and geopolitical fragmentation, precious metals have reclaimed their throne as the ultimate arbiters of value. The $4,500 gold and $72 silver marks are no longer just speculative targets; they are the benchmarks of a new economic era.

Moving forward, investors should closely monitor the "dot plot" of the Federal Reserve and the monthly reserve statements from the central banks of China and India. Any sign of a slowdown in BRICS accumulation could signal a cooling period for the market. However, as of December 25, 2025, the momentum belongs firmly to the bulls. The "Hard Asset Super-Cycle" is in full swing, and the financial world will never look the same.

This content is intended for informational purposes only and is not financial advice.