McLean, Virginia-based Capital One Financial Corporation (COF) is a financial services holding company with a market cap of $116.7 billion. It specializes in credit cards, consumer banking, commercial banking, and digital financial services.

Companies worth $10 billion or more are typically classified as “large-cap stocks,” and COF fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the credit services industry. The company has evolved into a uniquely vertically integrated powerhouse. Following its landmark acquisition of Discover and strategic tech buyouts, its strengths are now defined by its dual role as both a major bank and a global payments network.

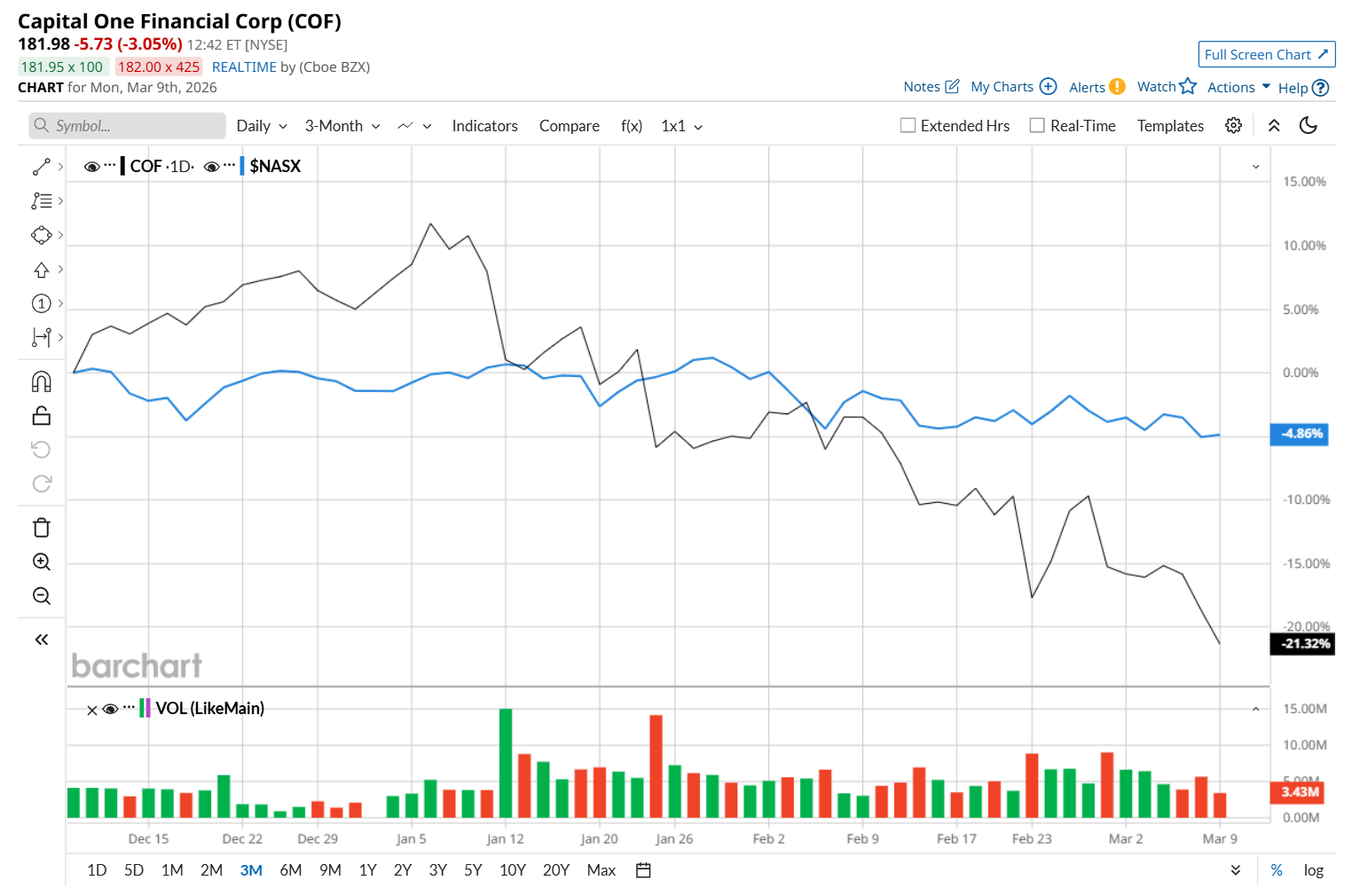

This financial company has slipped 30.1% from its 52-week high of $259.64, reached on Jan. 6. Shares of COF have declined 21.7% over the past three months, underperforming the Nasdaq Composite’s ($NASX) 5.2% drop during the same time frame.

Moreover, on a YTD basis, shares of COF are down 25.5%, compared to NASX’s 3.8% fall. In the longer term, COF has gained 4.3% over the past 52 weeks, trailing behind NASX’s 22.8% uptick over the same time frame.

To confirm its bearish trend, COF has been trading below its 200-day moving average since mid-February and has remained below its 50-day moving average since late January.

On Jan. 22, COF delivered its Q4 results, and its shares declined 7.6% in the following trading session. The company’s adjusted EPS of $3.86 missed analyst expectations of $4.14, while its efficiency ratio rose to 60%, significantly higher than the 52.5% analysts had projected, indicating that expenses increased faster than revenue. Although revenue of $15.6 billion slightly surpassed forecasts, weaker profitability led to the negative market reaction.

COF has underperformed its rival, American Express Company (AXP), which gained 9.2% over the past 52 weeks and declined 19.3% on a YTD basis.

Despite COF’s recent underperformance, analysts remain highly optimistic about its prospects. The stock has a consensus rating of "Strong Buy” from the 23 analysts covering it, and the mean price target of $277.95 suggests a 53.3% premium to its current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart