Micron Technology (MU) is a stock that is experiencing one of those periods where investors simply cannot turn away. RBC Capital Markets increased their target price for the memory leader to $525 a share from $425 while reiterating an “Outperform” rating. This is a major call, and it comes at a time when Micron Technology stock is already trading at fresh highs.

It is easy to see why this is such an optimistic call. Data centers are now the driving force behind memory demand growth, especially as high-bandwidth memory, or HBM, becomes an essential part of AI servers. This is also a call that assumes AI-related memory demand growth will be able to offset any potential weakness in PCs or smartphones. This is important because this memory super-cycle does not appear to be driven by PCs or smartphones as much as the previous memory super-cycles. Taken together, this is a much better setup for investors.

About Micron Stock

Micron Technology is a leading memory and storage chip manufacturer in the world. The company’s product lines include DRAM, NAND, NOR, solid-state drives, as well as high-bandwidth memory products. The company is based in Boise, Idaho. Today, the company’s market capitalization is about $497 billion. This is a number that indicates just how much sentiment for this stock has shifted.

At the current price of $456.20, MU is sitting just shy of its 52-week high of $458.28 after an incredible move from its 52-week low of $61.54. However, the valuation does not scream bubble just yet based on earnings. It’s currently trading for 40.16 times earnings but just 12.35 times forward earnings. That’s a big difference.

That tells me that Wall Street believes earnings are growing fast enough that they are going to compress the P/E. With a P/S of 12.83, the company is certainly not cheap based on revenue. But in a world where AI infrastructure stocks are getting rewarded as winners, this looks more reasonable than a number of software and accelerator stocks.

In other words, MU is no longer cheap but also not outlandish given the potential for this cycle to have legs all the way into 2027.

Micron Beat on Earnings, and the Guidance Was Even Better

The latest quarter for Micron has been a monster. For the company’s fiscal Q1 2026, the company reported $13.64 billion in revenue, an increase from $11.32 billion the prior quarter and $8.71 billion the prior year. GAAP diluted earnings per share came in at $4.60. Non-GAAP earnings per share came in at $4.78. And just as exciting was the non-GAAP gross margin expansion to 56.8%. And adjusted free cash flow? That came in at a record $3.9 billion. That’s not just growth. It's operating leverage.

Then came the guidance, and this probably had even greater significance. Micron provided their revenue estimate for fiscal Q2 2026, a figure of $18.7 billion with a variance of $400 million. The company also provided a non-GAAP EPS estimate of $8.42 and a gross margin of about 68%. These are huge numbers, and it looks like the company is continuing to move sharply upwards in terms of price and mix. Micron also began the quarter with $12 billion in cash, marketable investments, and restricted cash.

Of course, there is also some fresh product-related tailwind to this story. In fact, just this week, Micron announced that it has initiated high-volume production of its HBM4 36GB 12H product designed for Nvidia (NVDA) Vera Rubin systems, Gen6 SSD ramps, and SOCAMM2 ramps. That’s important because that’s precisely where this company needs to win in the marketplace—not just in commodity memory but in high-end AI content with limited supply and high margins.

One more thing that should be noted by investors is that this company has already announced that it will report fiscal Q2 2026 results after the market closes today, March 18. So, this company’s shares are not based upon some future event that may or may not materialize.

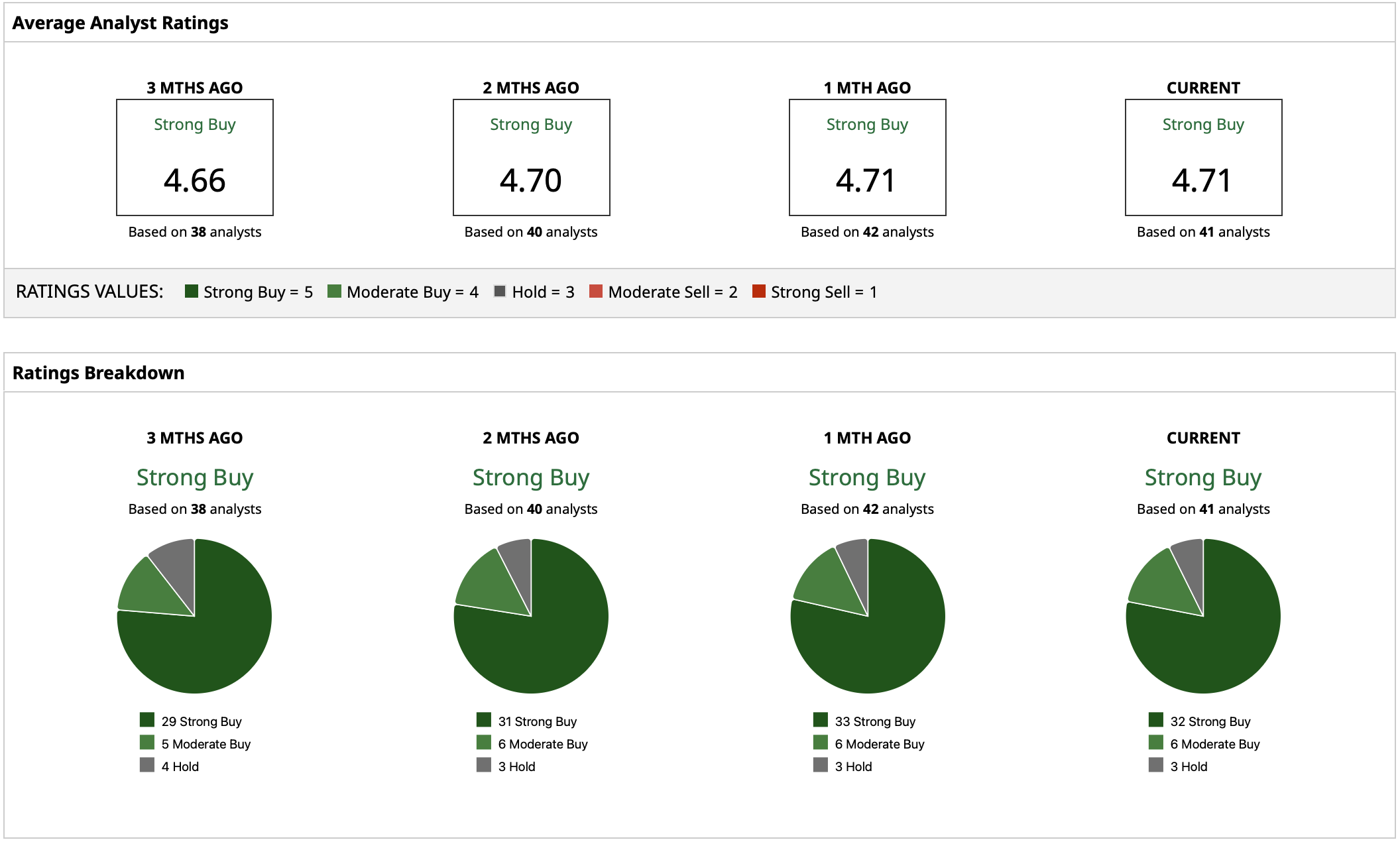

What Do Analysts Expect for MU Stock?

Wall Street is certainly bullish about this company’s prospects with a “Strong Buy” rating consensus. Although perhaps not as bullish as this stock’s current price suggests. In fact, just this week, RBC increased its target to $525 a share based upon its view that the memory upcycle remains intact and that AI-related demand will support memory prices at least through 2027.

MU’s mean analyst target is $387.38 a share, which is below its current trading price. Moreover, that figure represents a potential decline of 22% from its current trading price, although its street high target is $550 a share and represents a potential increase in its trading price of 17% from current levels.

On the date of publication, Yiannis Zourmpanos had a position in: MU . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dear Tesla Stock Fans, Mark Your Calendars for March 21

- Disney Gets a New Executive Team As 'Iger Era' Ends: Does That Make DIS Stock a Buy?

- Alibaba Earnings Preview: Should You Buy BABA Stock Now or Wait?

- Massive Meatpacking Strike: What Does It Mean for Beef Prices, Cattle as 3,800 Workers Go on Strike?