Wedbush analyst Dan Ives is a "permabull," and while that title has paid off in spades in the past few years, the fading software rally isn't a good look. The S&P 500 Software Index is down from its highs back in October 2025, but Ives still believes there's money to be made.

Speaking on CNBC, Ives said, "Right now, the Miami cab driver is bearish in software, and I think that's a bullish sign relative to where I see software this year." The implication is classic contrarian logic. This means that when bearishness on a sector becomes so pervasive that even people outside the industry are expressing it, the trade has likely become overcrowded on the short side.

The argument does have some rationale since the rest of the S&P 500 ($SPX) looks healthy. It's just software that has taken a beating.

Ives has doubled down on five stocks specifically, arguing that their decline now makes them prime buy-the-dip targets. Let's take a look at each of these software stocks.

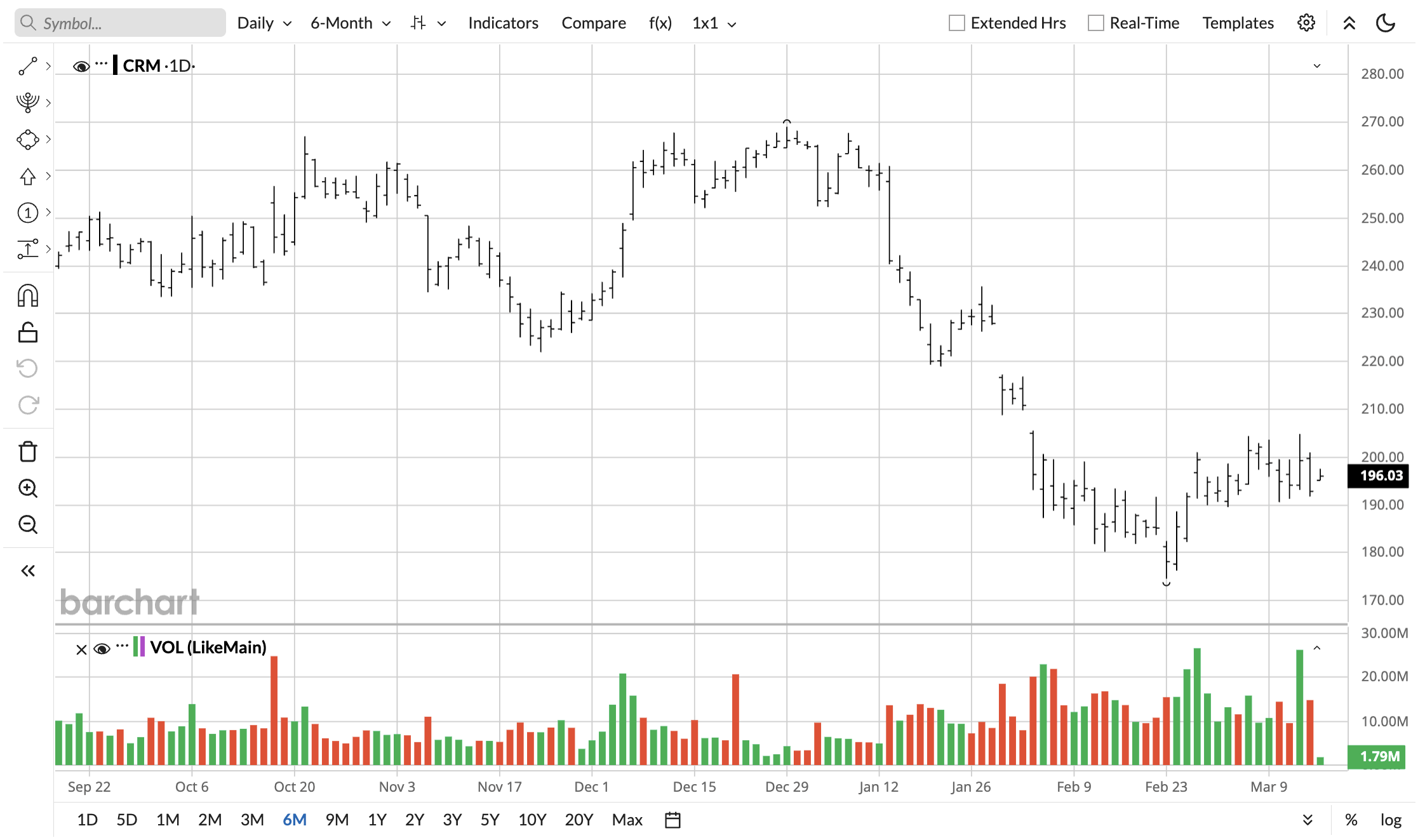

Software Stock #1: Salesforce (CRM)

Salesforce posted $11.2 billion in revenue, up 12% year-over-year (YOY), in the fourth quarter of fiscal 2026. This beat expectations, with EPS coming in at $3.81, a 25% positive surprise over the $3.05 consensus estimate. CEO Marc Benioff was characteristically defiant on the call, noting that wins over $1 million were up 26% YOY in Q4 and announcing a $50 billion share repurchase authorization. "These are some low prices," Benioff noted in regard to the repurchase authorization.

Salesforce returned more than $14 billion, or 99% of its free cash flow, to shareholders in fiscal 2026. Agentforce and Data 360 annual recurring revenue (ARR) grew by 200% YOY.

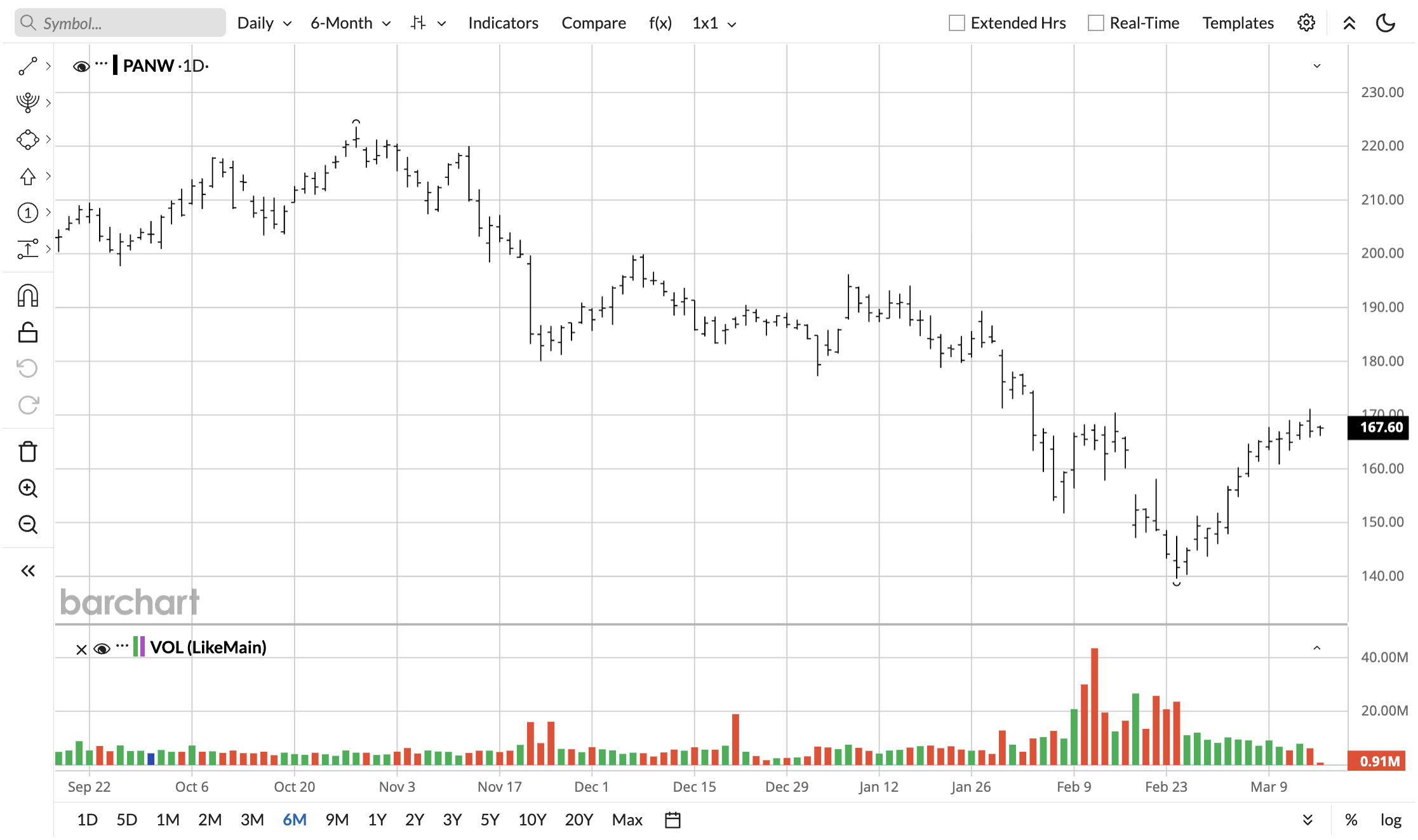

Software Stock #2: Palo Alto Networks (PANW)

Palo Alto Networks (PANW) is one of the biggest cybersecurity names. In Q2 fiscal 2026, its next-generation security ARR grew 33%. EPS came in at $1.03 versus expectations of $0.94, another beat.

Ives believes that Palo Alto Networks is sitting "squarely at the top of the cybersecurity mountain" and positioned to monetize the AI cybersecurity total addressable market over the next 12 to 18 months. In early March, the analyst listed PANW stock among his top 10 defensive technology names for navigating geopolitical volatility.

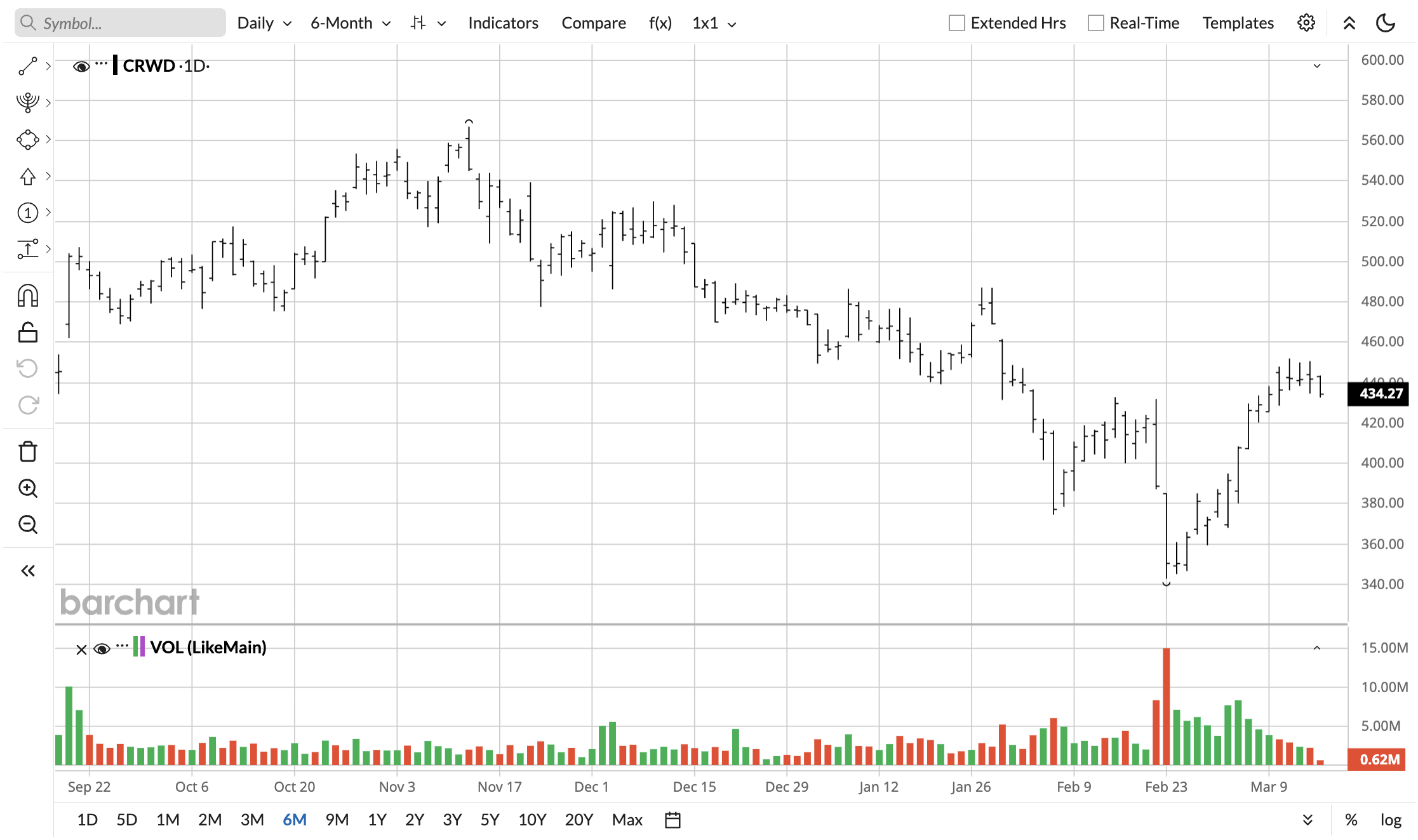

Software Stock #3: CrowdStrike (CRWD)

CrowdStrike (CRWD) posted one of the most impressive quarterly reports of the software stocks named by Dan Ives. In Q4 fiscal 2026, CrowdStrike reported an all-time record net new ARR of $331 million, up 47% YOY, and an ending ARR of $5.25 billion, up 24% YOY, making it the first pure-play cyber software company to surpass the $5 billion milestone.

Full-year net new ARR crossed $1 billion for the first time, up 25%, and record free cash flow hit $376 million for the quarter. Per CEO George Kurtz, AI is driving elevated demand for the Falcon platform while simultaneously “weaponizing adversaries to attack with increased speed, sophistication and precision.”

Ives believes that CrowdStrike's position as the “gold standard of cybersecurity” is still "firmly unchanged in the face of this Software Armageddon."

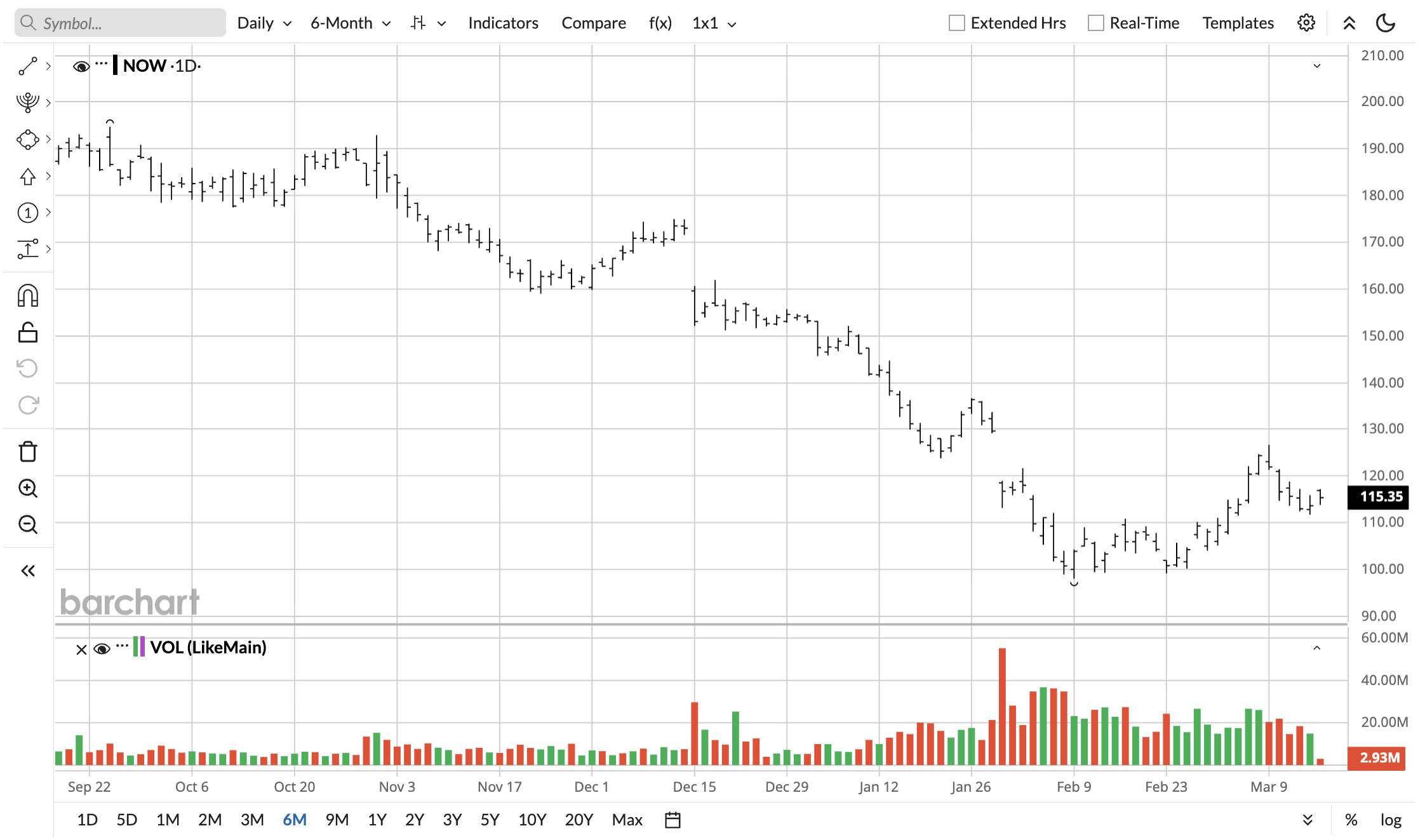

Software Stock #4: ServiceNow (NOW)

ServiceNow's (NOW) Q4 2025 earnings showed revenue and profitability above both internal guidance and analyst expectations, with accelerating growth in net new annual contract value (ACV) and AI-driven product lines. Now Assist, ServiceNow's AI product, surpassed $600 million in ACV and is tracking toward a $1 billion-plus target for 2026.

“ServiceNow has the fastest organic growth in the history of enterprise software. We're the fastest enterprise software company to have ever reached $1 billion, $5 billion, and $10 billion organically, and on our way to cross $15 billion-plus this year,” said ServiceNow CEO Bill McDermott.

According to Ives, ServiceNow is one of the platforms likely to benefit from AI adoption, with 30% of future AI spending potentially flowing to established software firms.

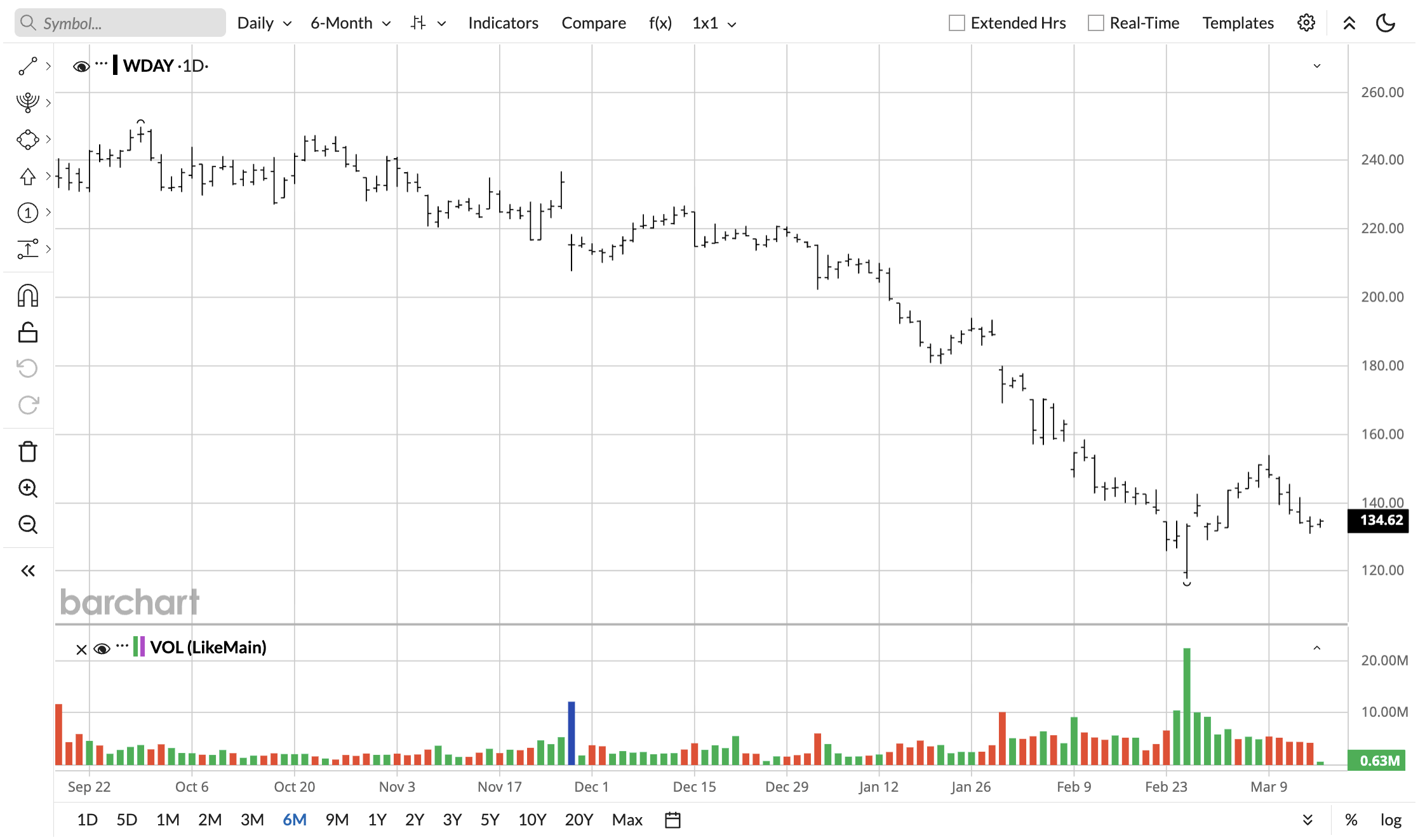

Software Stock #5: Workday (WDAY)

Workday (WDAY) posted Q4 fiscal 2026 EPS of $2.47, beating the estimate of $2.32. For the full year, the company posted over $100 million in new ACV from emerging AI products. That was reportedly double the figure from the same time last year.

CEO Aneel Bhusri pushed back directly against the narrative that AI will make HR and ERP software obsolete. "You've all heard the narrative out there that HR and ERP will be replaced or relegated to the background by AI. I personally just don't see that happening. Our application domains are really, really hard to build," said Bhusri.

WDAY stock is down significantly over the past year, falling 46% in the past 52 weeks, but the firm's quarterly numbers are anything but bearish.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 'The Miami Cab Driver Is Bearish on Software Stocks': Why You Should Buy the Dip in These 5 Oversold Names Now

- Delta Air Lines Just Broke Above Its 200-Day Moving Average. Should You Buy DAL Stock Here?

- Stop Fighting Time Decay: How Credit Spreads Change the Game for Options Traders

- Meta Platforms Just Delayed Its Avocado AI Rollout. Should You Sell META Stock?