Qualcomm (QCOM) stock is in the spotlight once again as Bank of America initiated coverage with an “Underperform” rating, indicating that the semiconductor and communications giant may not be able to achieve robust growth in the coming years. The company is facing difficulties in terms of its customer concentration and rising competition in the semiconductor industry.

Analyst Vivek Arya stated that Qualcomm is currently in a dominant position in terms of smartphone processor sales but indicated that the overall smartphone industry is maturing. Therefore, it is difficult for Qualcomm to achieve incremental sales in the coming years since its key customers are working toward developing their own chipsets. This warning is crucial for investors at a time when the semiconductor industry is highly competitive and dynamic in terms of technological advancements.

Qualcomm is currently working toward expanding its business in areas like automotive, Internet of Things (IoT), and artificial intelligence (AI) data center markets. However, it seems like these markets may not grow at a rate that is sufficient to compensate for Qualcomm’s declining business in its traditional segments like smartphones.

About Qualcomm Stock

Qualcomm is one of the leading semiconductor and telecommunications equipment companies in the world. It is headquartered in San Diego, California. The company is currently working toward designing and selling system-on-chip processors and modem chips for use in smartphones and other devices. Its products are used in various industries like automotive, industrial, and Internet of Things (IoT) markets.

Qualcomm is currently one of the most dominant semiconductor companies in the world, with a market capitalization of around $143 billion. QCOM stock is has traded between roughly $120 and $205 over the last 12 months. It is currently trading at the lower end of that range and is performing worse compared to its semiconductor peers.

Valuation metrics indicate that Qualcomm is not overvalued compared to other semiconductor stocks. It has a trailing price-to-earnings (P/E) multiple of 13.8x and a forward P/E of 16.2x. Meanwhile, its sales multiple is 3.33x. Qualcomm also has a P/E-to-growth multiple of 6.9x, indicating that it has limited growth potential compared to other chipmakers.

Qualcomm Reports Mixed Fiscal Q1 Results

Qualcomm recently announced fiscal first-quarter 2026 revenue of $12.25 billion, representing a 5% increase from fiscal first-quarter 2025 results. However, its profitability has shown mixed results. Its GAAP net income declined by 6% compared to fiscal first-quarter 2025 results. Its diluted earnings per share (EPS) also declined slightly to $2.78.

On the other hand, its non-GAAP EPS results showed a 3% increase to $3.50. Its semiconductor segment results, known as QCT, generated $10.6 billion in revenue during fiscal first-quarter 2026, driven by continued demand for mobile chipsets.

Its handsets revenue grew by 3% to $7.82 billion. Its automotive revenue grew by 15% to $1.1 billion as it continues to expand its presence in connected vehicles. IoT revenue also grew by 9% to $1.69 billion as IoT devices increasingly require connectivity.

However, it has also mentioned that smartphone demand is still impacted by memory supply constraints and higher component costs. It is expected to impact its handsets shipments going forward.

Structural Risks in Qualcomm’s Core Business

Bank of America’s downgrade is largely centered around structural risks in Qualcomm’s main business. One of the biggest risks is Qualcomm’s gradual loss of business with Apple (AAPL), which would eliminate an estimated $7 billion to $8 billion in annual revenue, as Apple makes a complete transition to in-house chips.

Qualcomm is also dealing with changing dynamics in its business with other large smartphone manufacturers. Samsung is reportedly cutting Qualcomm’s share of Galaxy smartphone chips from 100% to about 75%. Another smartphone manufacturer, Xiaomi (XIACY), is significantly increasing spending on in-house semiconductor design.

Qualcomm is also dealing with increasing DRAM costs due to demand from AI servers. The company's increasing costs could impact the smartphone supply chain. These costs may impact handset production, especially in price-sensitive markets such as China.

Long-term, Qualcomm is facing increasing competition in every business segment it is attempting to diversify into. Competition is increasing in its attempts to grow in the premium smartphone chip business, especially against MediaTek. Qualcomm is also facing increasing competition in automotive computing chips from Nvidia (NVDA) and Mobileye (MBLY).

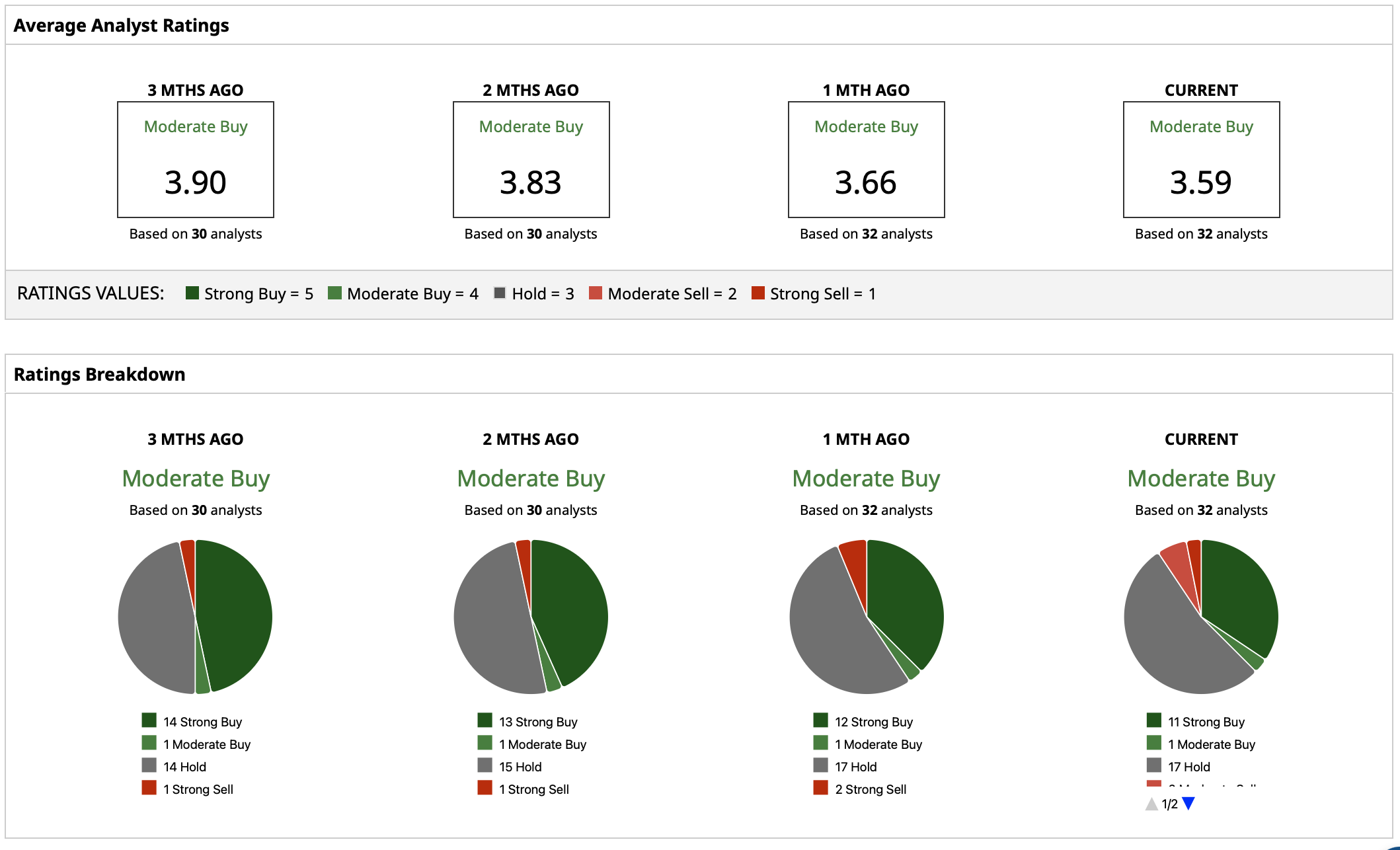

What Do Analysts Expect for Qualcomm Stock?

Although Bank of America is bearish on Qualcomm stock, Wall Street’s expectations are generally balanced, with a “Moderate Buy” consensus rating and a mean price target of $164.69. This represents potential upside of about 22% as Qualcomm successfully executes its business diversification strategy and maintains profitability in its main business.

However, analysts’ estimates vary significantly. Qualcomm’s stock is currently being given a high estimate of $205 and a low estimate of $132.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Nvidia Launches Its Nemotron 3 AI Model, Should You Buy, Sell, or Hold NVDA Stock?

- Memory Pricing Is Still Hot, Creating a Prolonged Buying Opportunity in Micron Stock

- Google Just Closed Its $32 Billion Wiz Deal. How Should You Play GOOGL Stock Here?

- Qualcomm Stock Warning: Why Bank of America Is Betting That QCOM Will Underperform