Diamondback Energy, Inc. (FANG), headquartered in Midland, Texas, operates as an independent oil and natural gas company. With a market cap of $48.4 billion, the company acquires, develops, explores, and exploits unconventional, onshore oil and natural gas reserves in the Permian Basin in West Texas.

Shares of this leading independent oil and gas company have underperformed the broader market over the past year. FANG has gained 8.3% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 11.8%. However, in 2026, FANG stock is up 12.5%, surpassing the SPX’s marginal fall on a YTD basis.

Narrowing the focus, FANG’s underperformance is also apparent compared to the iShares U.S. Oil & Gas Exploration & Production ETF (IEO). The exchange-traded fund has gained about 12.8% over the past year. Moreover, the ETF’s 18.3% returns on a YTD basis outshine the stock’s gains over the same time frame.

FANG's underperformance is due to weaker oil pricing, with the company's realized oil price down 11.7% to $64.60 per barrel. Management prioritized debt reduction and cash returns over expanding output, keeping oil volumes flat.

On Nov. 3, 2025, FANG shares closed down by 1.3% after reporting its Q3 results. Its adjusted EPS of $3.08 beat Wall Street expectations of $2.85. The company’s revenue was $3.9 billion, surpassing Wall Street forecasts of $3.5 billion.

For the current fiscal year, ended in December 2025, analysts expect FANG’s EPS to decline 25.5% to $12.34 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

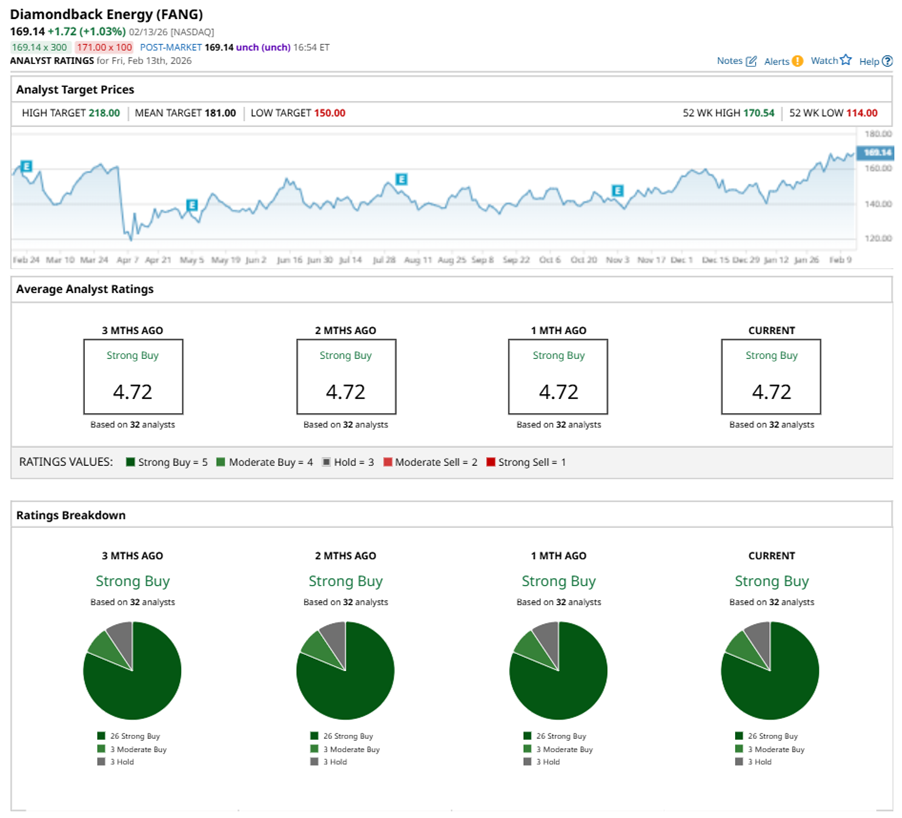

Among the 32 analysts covering FANG stock, the consensus is a “Strong Buy.” That’s based on 26 “Strong Buy” ratings, three “Moderate Buys,” and three “Holds.”

The configuration has been consistent over the past three months.

On Feb. 13, Bob Brackett from Bernstein maintained a “Buy” rating on FANG with a price target of $190, implying a potential upside of 12.3% from current levels.

The mean price target of $181 represents a 7% premium to FANG’s current price levels. The Street-high price target of $218 suggests an upside potential of 28.9%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart