Over the past six months, CoreCivic’s stock price fell to $18.66. Shareholders have lost 7.3% of their capital, which is disappointing considering the S&P 500 has climbed by 8.2%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in CoreCivic, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think CoreCivic Will Underperform?

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons you should be careful with CXW and a stock we'd rather own.

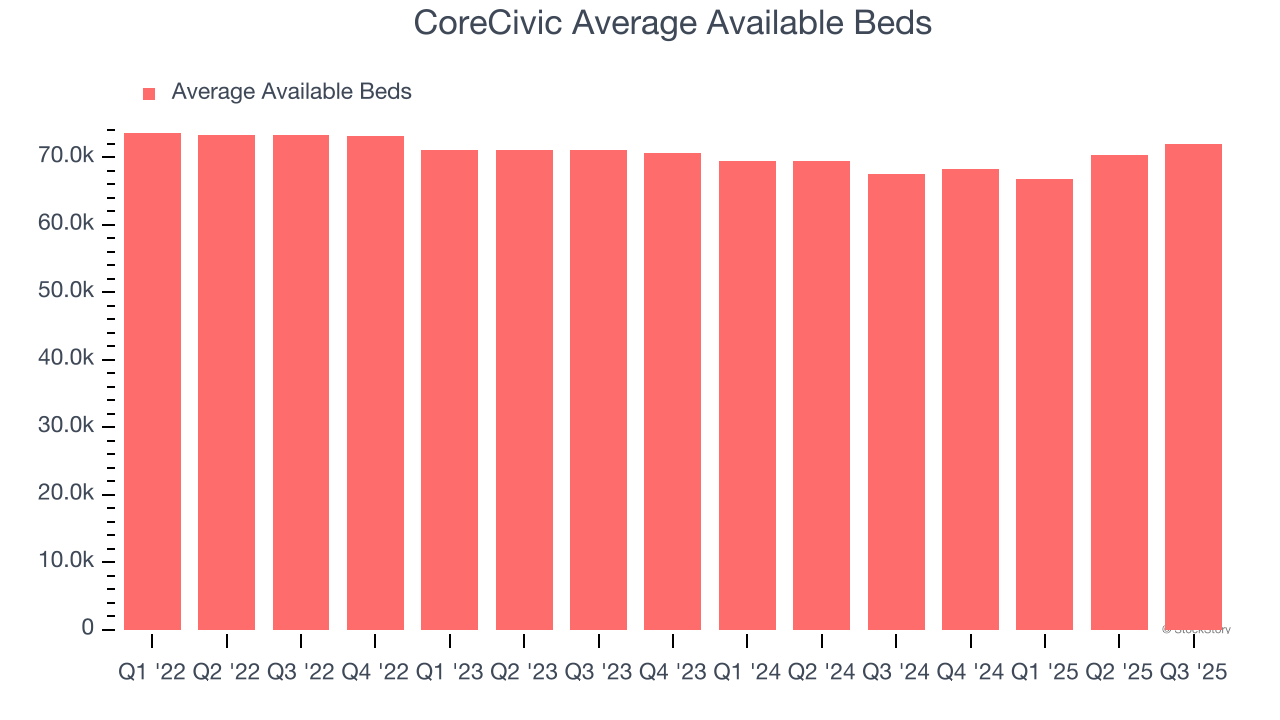

1. Decline in Average available beds Points to Weak Demand

Revenue growth can be broken down into changes in price and volume (for companies like CoreCivic, our preferred volume metric is average available beds ). While both are important, the latter is the most critical to analyze because prices have a ceiling.

CoreCivic’s average available beds

came in at 71,996 in the latest quarter, and over the last two years, averaged 1.6% year-on-year declines. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests CoreCivic might have to lower prices or invest in product improvements to grow, factors that can hinder near-term profitability.

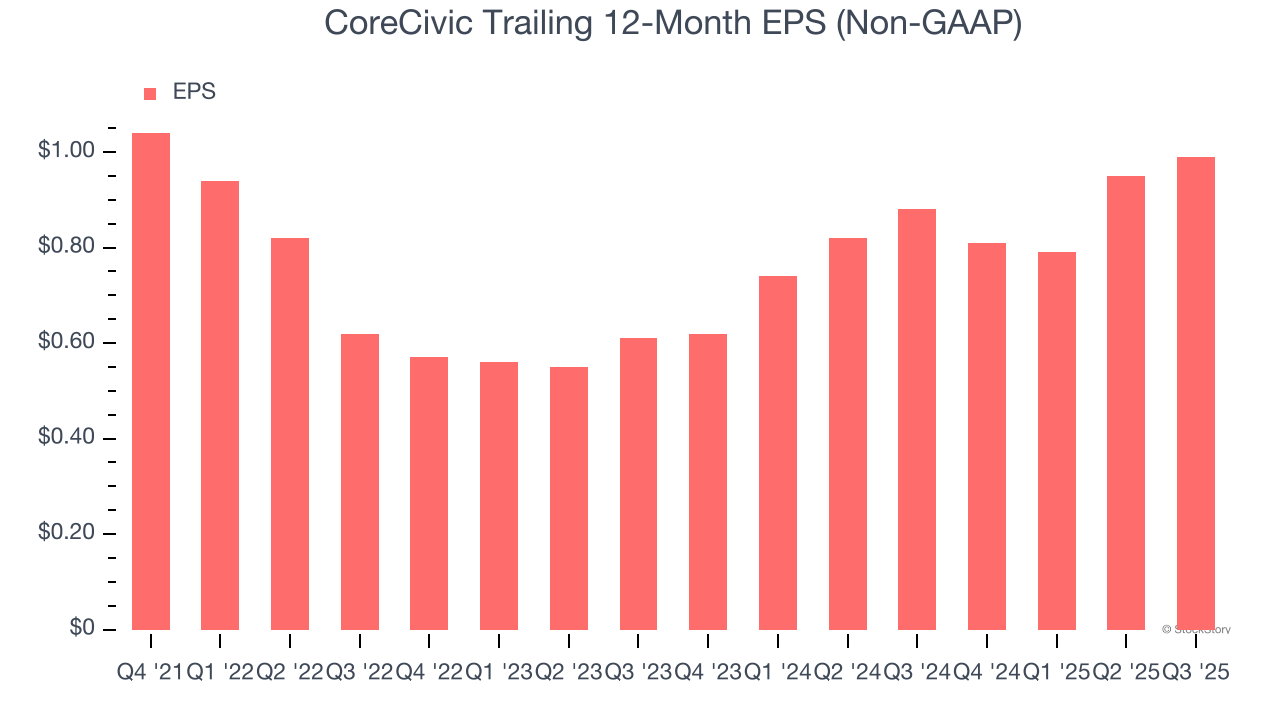

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

CoreCivic’s full-year EPS grew at a weak 1.9% compounded annual growth rate over the last four years, worse than the broader business services sector.

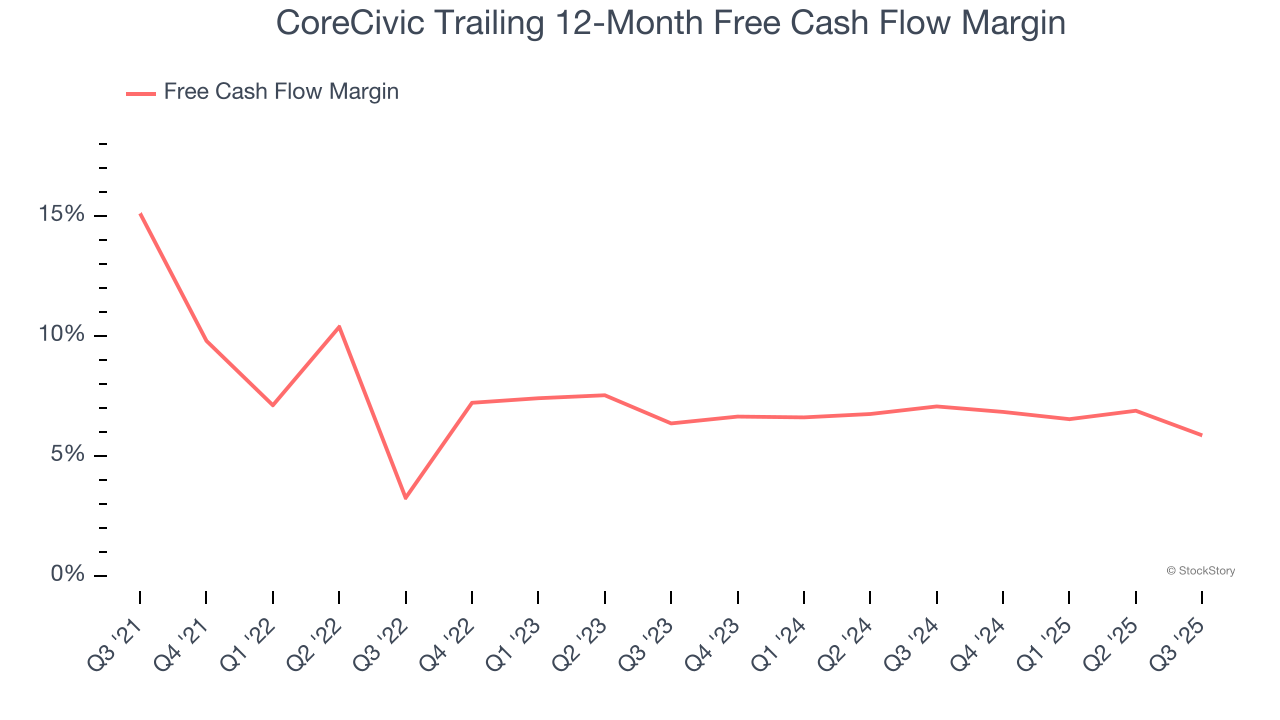

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, CoreCivic’s margin dropped by 9.2 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. CoreCivic’s free cash flow margin for the trailing 12 months was 5.9%.

Final Judgment

We cheer for all companies making their customers lives easier, but in the case of CoreCivic, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 15.5× forward P/E (or $18.66 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. We’d suggest looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.