DocuSign’s stock price has taken a beating over the past six months, shedding 21.1% of its value and falling to $69.33 per share. This might have investors contemplating their next move.

Is there a buying opportunity in DocuSign, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is DocuSign Not Exciting?

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons why we avoid DOCU and a stock we'd rather own.

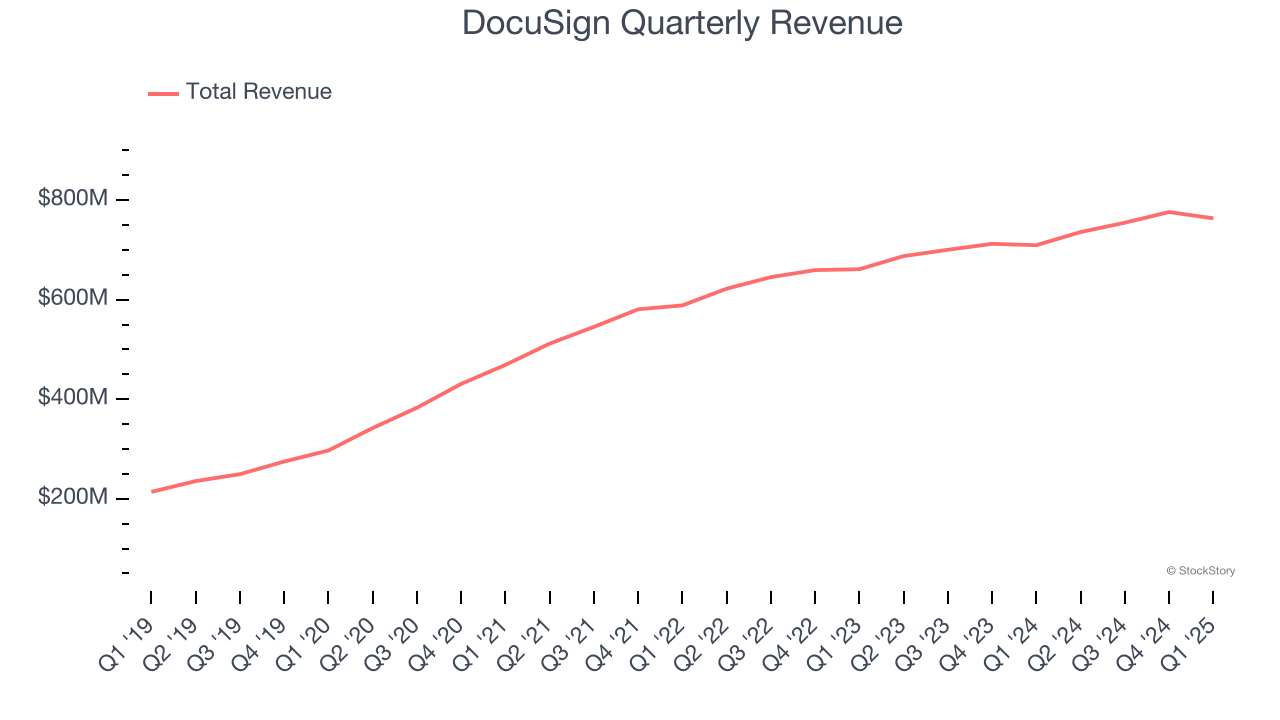

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, DocuSign grew its sales at a 10.8% annual rate. Although this growth is acceptable on an absolute basis, it fell short of our standards for the software sector, which enjoys a number of secular tailwinds.

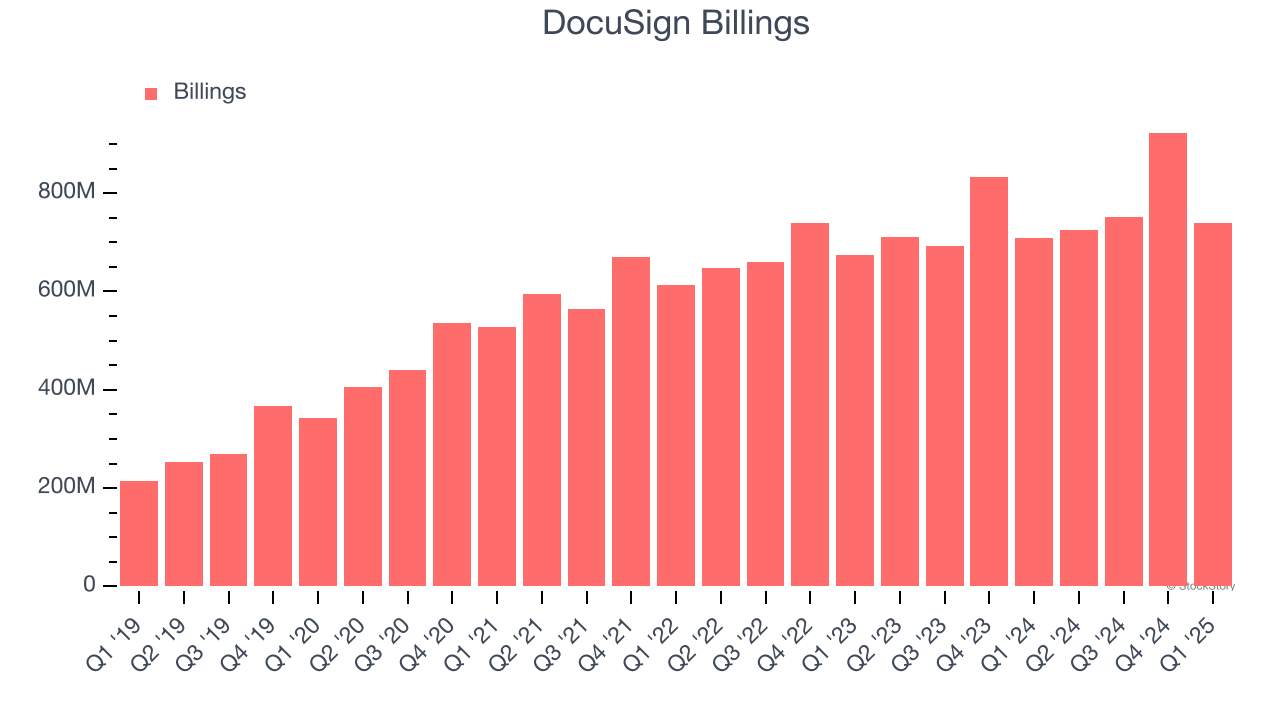

2. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

DocuSign’s billings came in at $739.6 million in Q1, and over the last four quarters, its year-on-year growth averaged 6.4%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect DocuSign’s revenue to rise by 5.9%, a deceleration versus This projection doesn't excite us and indicates its products and services will face some demand challenges.

Final Judgment

DocuSign isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 4.6× forward price-to-sales (or $69.33 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward the Amazon and PayPal of Latin America.

High-Quality Stocks for All Market Conditions

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.