Fast-food chain Wingstop (NASDAQ: WING) reported Q2 CY2025 results topping the market’s revenue expectations, with sales up 12% year on year to $174.3 million. Its non-GAAP profit of $1 per share was 15.1% above analysts’ consensus estimates.

Is now the time to buy Wingstop? Find out by accessing our full research report, it’s free.

Wingstop (WING) Q2 CY2025 Highlights:

- Revenue: $174.3 million vs analyst estimates of $173.4 million (12% year-on-year growth, 0.5% beat)

- Adjusted EPS: $1 vs analyst estimates of $0.87 (15.1% beat)

- Adjusted EBITDA: $59.21 million vs analyst estimates of $56.86 million (34% margin, 4.1% beat)

- Operating Margin: 25.9%, in line with the same quarter last year

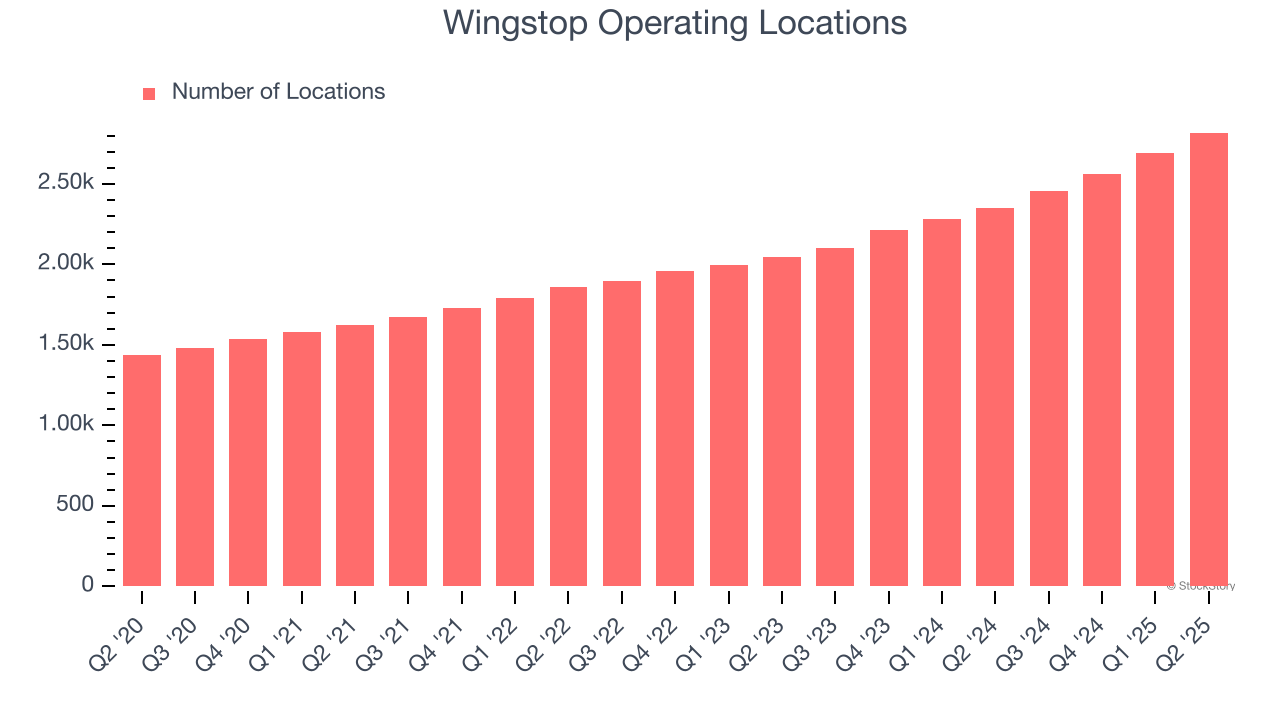

- Locations: 2,818 at quarter end, up from 2,352 in the same quarter last year

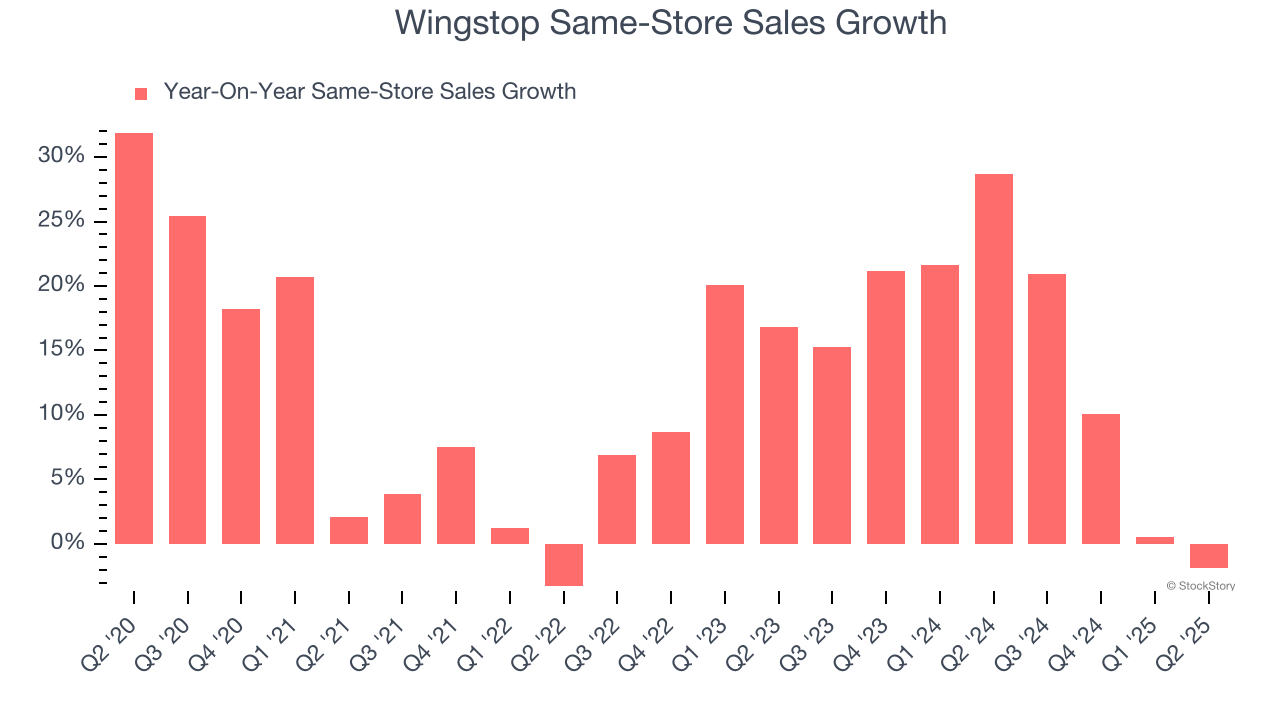

- Same-Store Sales fell 1.9% year on year (28.7% in the same quarter last year)

- Market Capitalization: $8.1 billion

"Our second quarter results showcase the strength of our unit economics and returns our brand partners are seeing for their businesses," said Michael Skipworth, President & Chief Executive Officer.

Company Overview

The passion project of two chicken wing aficionados in Texas, Wingstop (NASDAQ: WING) is a popular fast-food chain known for its flavorful and crispy chicken wings offered in a variety of sauces and seasonings.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $669.7 million in revenue over the past 12 months, Wingstop is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, Wingstop’s 25% annualized revenue growth over the last six years (we compare to 2019 to normalize for COVID-19 impacts) was incredible as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Wingstop reported year-on-year revenue growth of 12%, and its $174.3 million of revenue exceeded Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 18.4% over the next 12 months, a deceleration versus the last six years. Still, this projection is admirable and indicates the market sees success for its menu offerings.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Restaurant Performance

Number of Restaurants

Wingstop operated 2,818 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 15.4% annual growth, much faster than the broader restaurant sector. This gives it a chance to scale into a mid-sized business over time. Furthermore, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Wingstop provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Wingstop has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 14.6%. This performance along with its meaningful buildout of new restaurants suggest it’s playing some aggressive offense.

In the latest quarter, Wingstop’s same-store sales fell by 1.9% year on year. This decline was a reversal from its historical levels. A one quarter hiccup shouldn’t deter you from investing in a business, and we’ll be monitoring the company to see how things progress.

Key Takeaways from Wingstop’s Q2 Results

We were impressed by how significantly Wingstop blew past analysts’ same-store sales expectations this quarter. We were also glad its EPS and EBITDA outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 20.8% to $351.38 immediately following the results.

Wingstop put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.