Old Republic International has followed the market’s trajectory closely, rising in tandem with the S&P 500 over the past six months. The stock has climbed by 18% to $44.15 per share while the index has gained 14.4%.

Is now the time to buy Old Republic International, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Is Old Republic International Not Exciting?

We don't have much confidence in Old Republic International. Here are three reasons why ORI doesn't excite us and a stock we'd rather own.

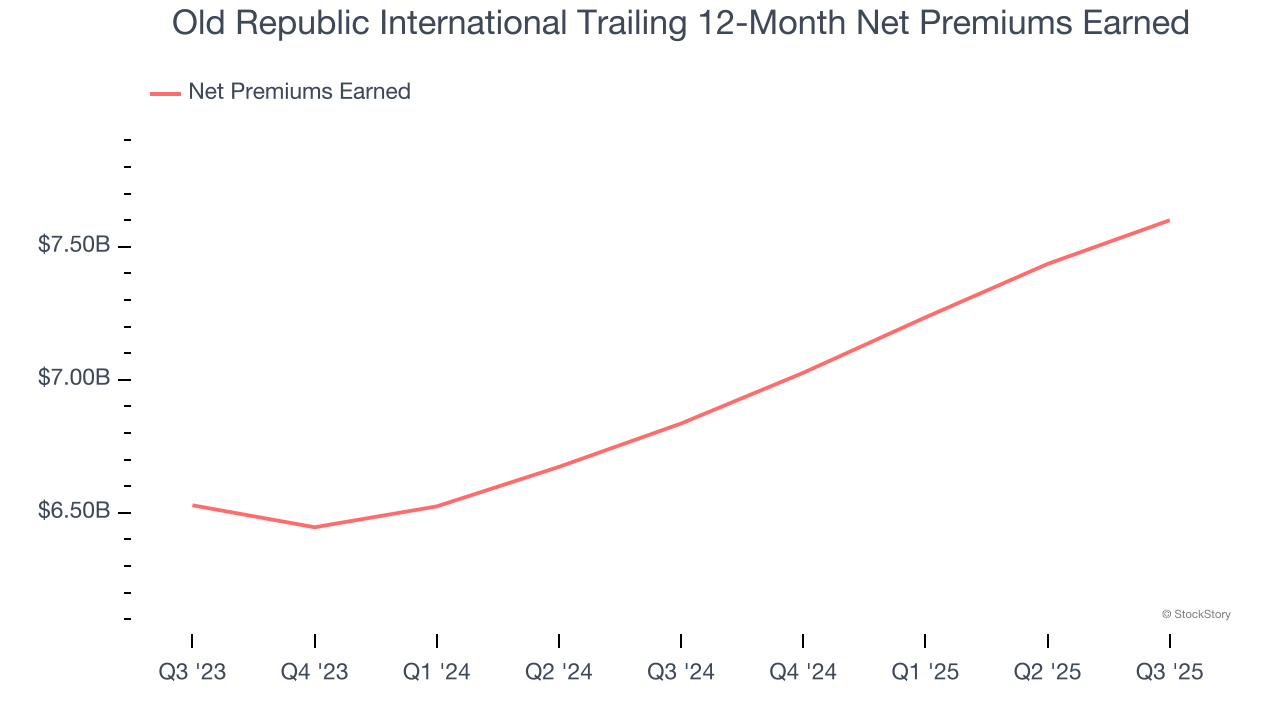

1. Net Premiums Earned Point to Soft Demand

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

Old Republic International’s net premiums earned has grown at a 3.3% annualized rate over the last five years, worse than the broader insurance industry and slower than its total revenue.

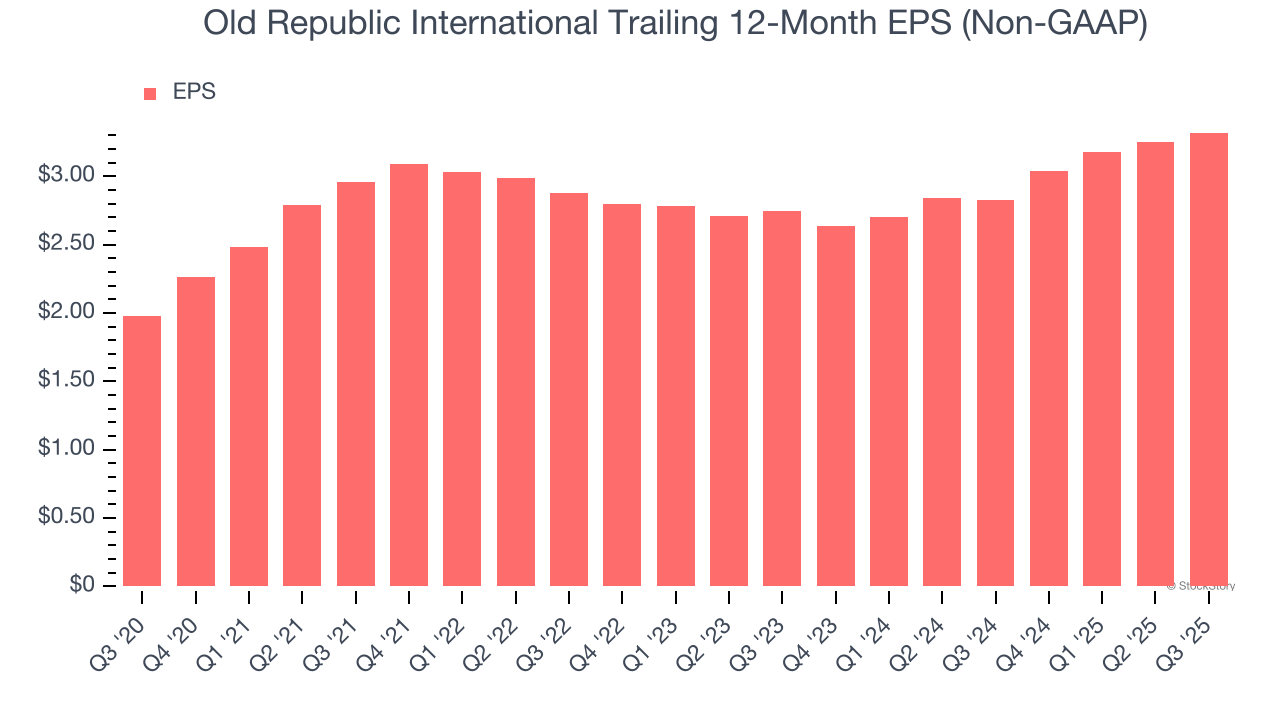

2. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Old Republic International’s EPS grew at a weak 9.9% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 6.9% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

3. BVPS Projections Show Stormy Skies Ahead

An insurer’s book value per share (BVPS) increases when it maintains a profitable combined ratio and effectively manages its investment portfolio.

Over the next 12 months, Consensus estimates call for Old Republic International’s BVPS to shrink by 1% to $24.35, a sour projection.

Final Judgment

Old Republic International isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 1.7× forward P/B (or $44.15 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.