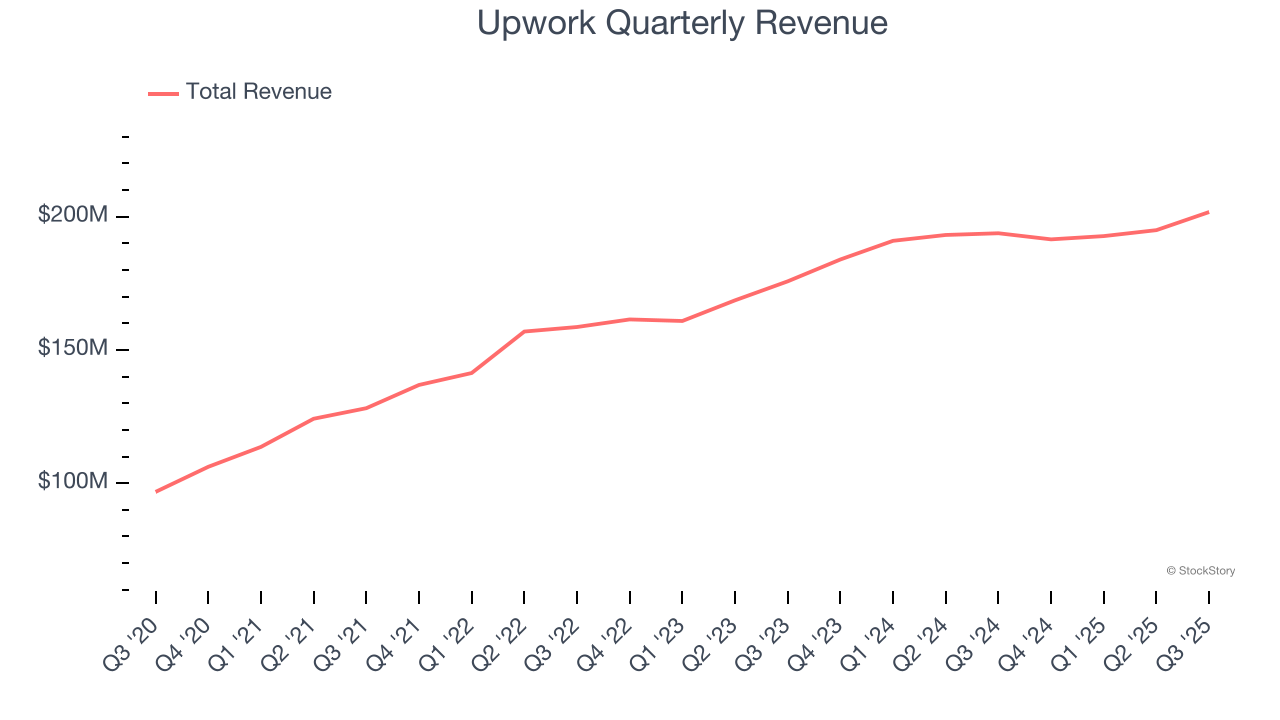

Online work marketplace Upwork (NASDAQ: UPWK) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 4.1% year on year to $201.7 million. Guidance for next quarter’s revenue was better than expected at $195.5 million at the midpoint, 1.7% above analysts’ estimates. Its non-GAAP profit of $0.36 per share was 25.9% above analysts’ consensus estimates.

Is now the time to buy Upwork? Find out by accessing our full research report, it’s free for active Edge members.

Upwork (UPWK) Q3 CY2025 Highlights:

- Revenue: $201.7 million vs analyst estimates of $193.4 million (4.1% year-on-year growth, 4.3% beat)

- Adjusted EPS: $0.36 vs analyst estimates of $0.29 (25.9% beat)

- Adjusted EBITDA: $59.63 million vs analyst estimates of $50.12 million (29.6% margin, 19% beat)

- Revenue Guidance for Q4 CY2025 is $195.5 million at the midpoint, above analyst estimates of $192.2 million

- Management raised its full-year Adjusted EPS guidance to $1.36 at the midpoint, a 17.2% increase

- EBITDA guidance for the full year is $223.5 million at the midpoint, above analyst estimates of $212.7 million

- Operating Margin: 14.8%, up from 10.7% in the same quarter last year

- Free Cash Flow Margin: 34.4%, similar to the previous quarter

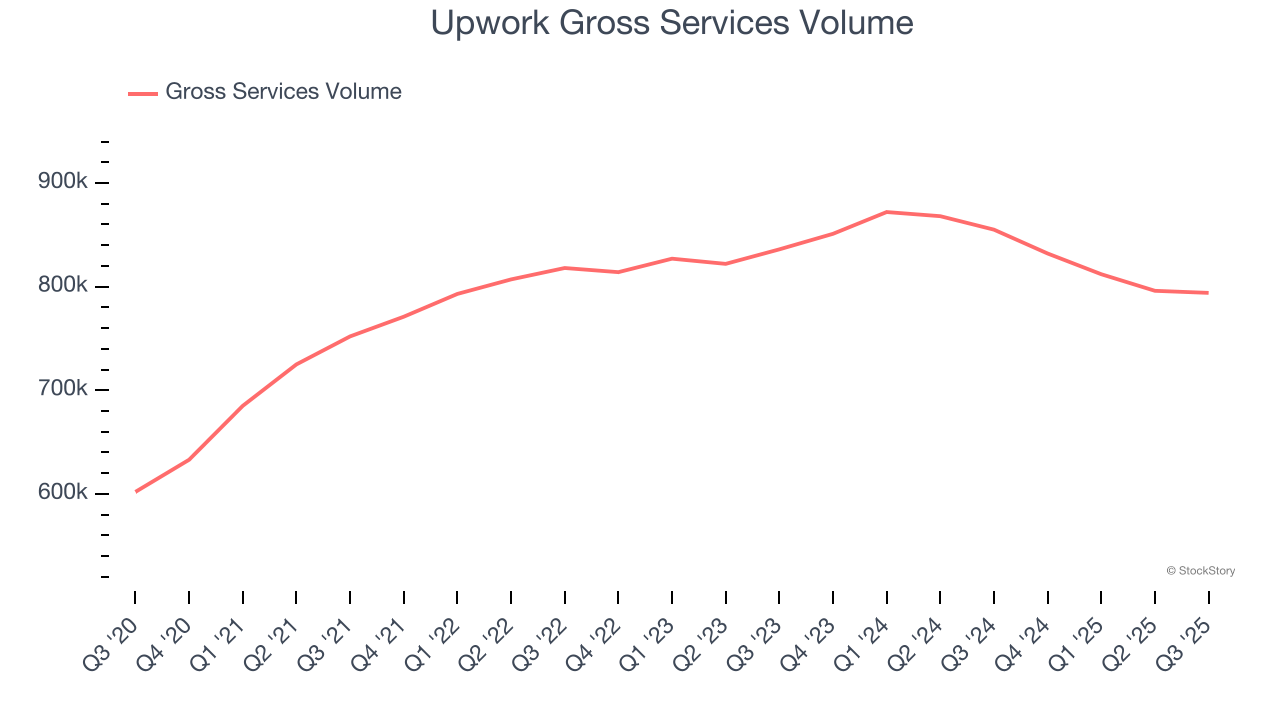

- Gross Services Volume: 794,000, down 61,000 year on year

- Market Capitalization: $2.11 billion

“The third quarter marked the start of the next chapter for Upwork. As we build the world’s human and AI-powered work marketplace, we’re driving phenomenal user productivity and engagement, resulting in a return to positive GSV growth,” said Hayden Brown, president and CEO, Upwork Inc.

Company Overview

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ: UPWK) is an online platform where businesses and independent professionals connect to get work done.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Upwork’s sales grew at a mediocre 9.6% compounded annual growth rate over the last three years. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Upwork.

This quarter, Upwork reported modest year-on-year revenue growth of 4.1% but beat Wall Street’s estimates by 4.3%. Company management is currently guiding for a 2.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Gross Services Volume

Customer Growth

As a gig economy marketplace, Upwork generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Upwork struggled with new customer acquisition over the last two years as its gross services volume were flat at 794,000. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Upwork wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

In Q3, Upwork’s gross services volume decreased by 61,000, a 7.1% drop since last year. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t moving the needle for customers yet.

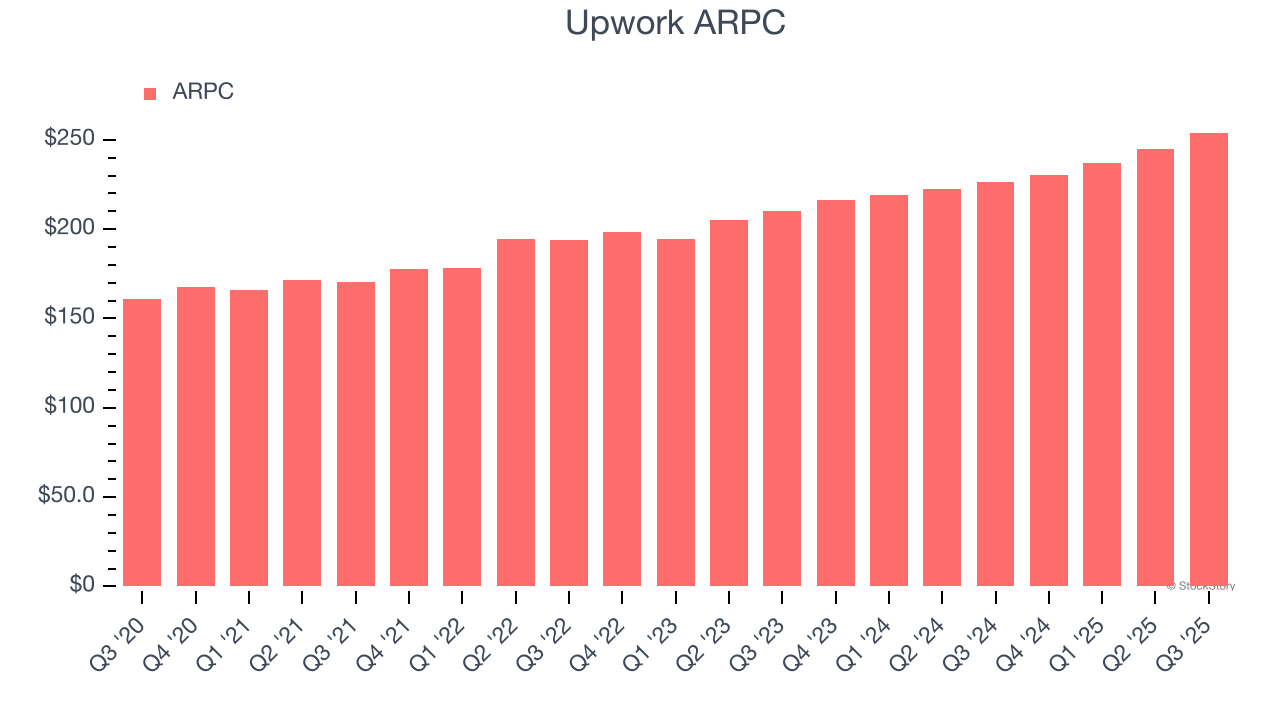

Revenue Per Customer

Average revenue per customer (ARPC) is a critical metric to track because it measures how much the company earns in transaction fees from each customer. This number also informs us about Upwork’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

Upwork’s ARPC growth has been excellent over the last two years, averaging 9.4%. Although its gross services volume were flat during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing customers.

This quarter, Upwork’s ARPC clocked in at $254.07. It grew by 12.1% year on year, faster than its gross services volume.

Key Takeaways from Upwork’s Q3 Results

Revenue beat, which is a good start. We were also impressed by how significantly Upwork blew past analysts’ EBITDA expectations this quarter. Looking ahead, the company's full-year EBITDA guidance trumped Wall Street’s estimates and full-year EPS guidance was raised. Overall, we think this was a very solid quarter with some key areas of upside. The stock traded up 14.9% to $17.95 immediately following the results.

Upwork had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.