The global financial landscape underwent a violent recalibration this month following the formal nomination of Kevin Warsh to succeed Jerome Powell as the Chair of the Federal Reserve. Dubbed the "Warsh Shock" by traders, the announcement on January 30, 2026, has triggered a massive de-risking event across asset classes, signaling the definitive end of the "easy money" era and the birth of a new "Sound Money" regime.

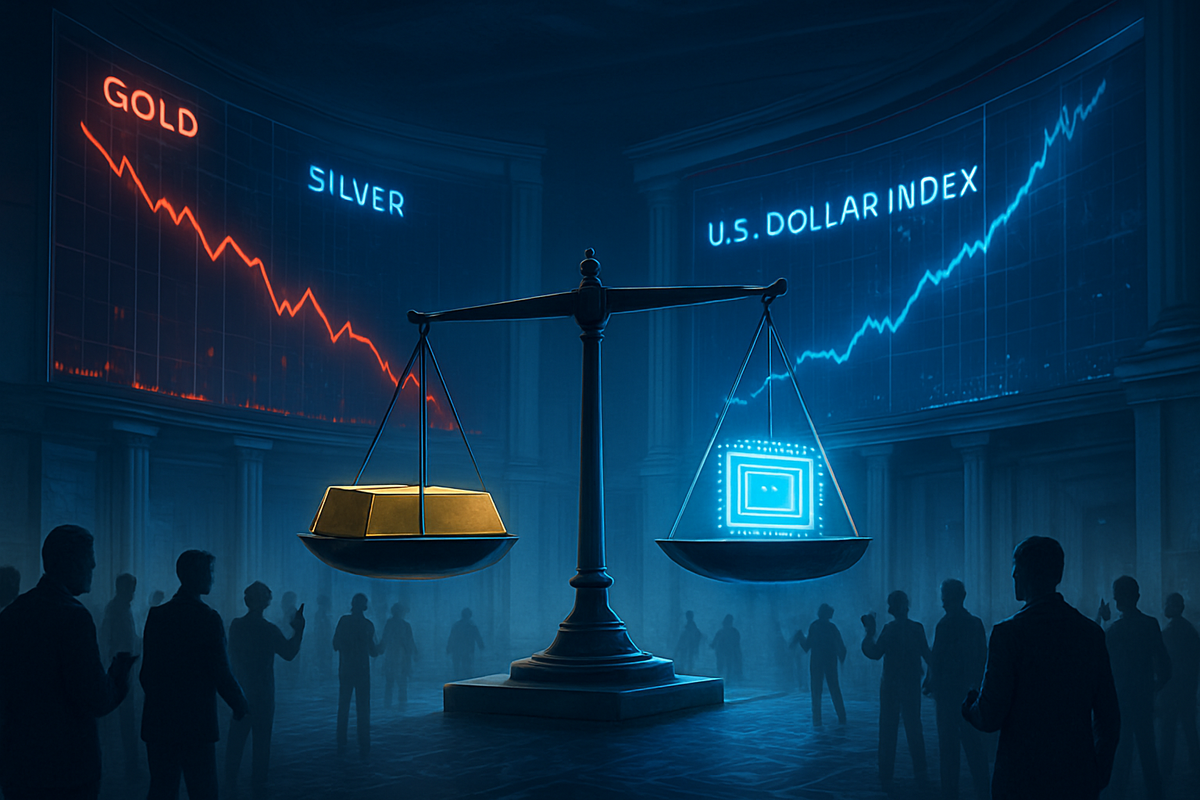

As of February 13, 2026, the markets are still grappling with the implications of a Fed leader who promises to aggressively shrink the central bank's $6.6 trillion balance sheet while simultaneously betting on an artificial intelligence-driven productivity boom to keep inflation in check. This "Warshian" philosophy—a complex blend of hard-money hawkishness and growth-oriented dovishness—has sent the U.S. Dollar Index (DXY) to multi-year highs and forced a painful unwinding of the long-standing "debasement trade."

A New Sheriff in Town: The Anatomy of the Shock

The nomination of Kevin Warsh was not merely a change in leadership; it was a signal of a fundamental regime shift in monetary policy. For years, the market had operated under the assumption of the "Fed Put"—the belief that the central bank would intervene to support equity markets during significant downturns. With Warsh’s selection, analysts from firms like Citadel Securities suggest that the strike price of that put has effectively dropped to zero. The immediate reaction was a "Great Metal Flush," with gold prices suffering a historic flash crash, dropping nearly 10% in a single day, while silver plunged by 30% as investors abandoned hedges against currency debasement.

The timeline leading to this moment began in late 2025, as speculation mounted over Powell’s successor. While traditional candidates favored a continuation of "data-dependent" gradualism, the administration’s choice of Warsh signaled a desire for a "narrow central bank" remit. Since the announcement, the 10-year Treasury yield has spiked to 4.28%, driven by expectations that the Fed will no longer "coddle" the bond market through heavy intervention or the purchase of mortgage-backed securities (MBS).

Key stakeholders, including institutional investors and global central banks, are now scrambling to adjust to Warsh’s "Monetary Barbell" strategy. This approach seeks to balance aggressive Quantitative Tightening (QT) with a willingness to keep interest rates lower—targeting a 2.75% to 3.25% range—provided that productivity gains from AI continue to suppress inflationary pressures. It is a high-stakes gamble that the private sector, rather than central bank liquidity, should be the primary engine of economic expansion.

Winners and Losers in the New Regime

The "Warsh Shock" has created a stark divide between industries that thrived on liquidity and those poised to benefit from a steeper yield curve and deregulation. The primary beneficiaries have been the "Too Big to Fail" banks. JPMorgan Chase & Co. (NYSE: JPM) and Goldman Sachs Group Inc. (NYSE: GS) saw their share prices surge as investors anticipated a "bear steepener" in the yield curve, which expands net interest margins (NIM) for traditional lenders. Furthermore, Warsh’s vocal criticism of the "Basel III Endgame" capital requirements suggests a regulatory thaw that could free up billions of dollars for share buybacks and dividends.

Conversely, the "mining meltdown" has devastated traditional inflation hedges. Companies like Newmont Corporation (NYSE: NEM) and Barrick Gold Corp (NYSE: GOLD) faced a brutal sell-off as the dollar re-anchored as a credible store of value. The cryptocurrency sector was not spared either; Bitcoin (BTC) and related digital assets entered a sharp bear market as the "oxygen" of abundant speculative liquidity was restricted, with the premier cryptocurrency sliding toward the $80,000 range.

The technology sector remains a divided battlefield. High-multiple growth stocks and companies reliant on cheap debt have slumped. However, "productivity plays" like Nvidia Corp (NASDAQ: NVDA) and Microsoft Corp (NASDAQ: MSFT) have shown resilience. Because the Warsh thesis relies on AI to drive structural disinflation, these firms are increasingly viewed as the structural winners of a "New Economy" where growth must be earned through efficiency rather than funded by the printing press.

The End of the "Fed Put" and the Rise of Productivity

The wider significance of the Warsh nomination lies in its challenge to the prevailing central banking orthodoxy of the last two decades. By advocating for a "leaner Fed," Warsh is attempting to untangle the central bank from the inner workings of the financial "plumbing." His priority to exit the MBS market entirely and reform the "ample reserves" system is a direct assault on the policies that many critics argue have distorted price discovery and encouraged excessive risk-taking.

This event fits into a broader global trend of "reshoring" and "sound money" advocacy that has gained momentum in the mid-2020s. The ripple effects are already being felt by international partners; a stronger dollar is putting immense pressure on emerging markets that carry high dollar-denominated debt. Historically, the "Warsh Shock" draws comparisons to the Volcker era of the early 1980s, though with a modern twist: while Volcker used high rates to crush inflation, Warsh intends to use a smaller balance sheet to restore market discipline while using AI-led growth as his primary shield against a recession.

Regulatory implications are equally profound. A Warsh-led Fed is expected to be significantly more skeptical of climate-related financial disclosures and other "mission creep" initiatives that have expanded under previous leadership. This shift back to a singular focus on monetary stability and bank solvency is expected to simplify the operating environment for the financial sector but may draw fire from progressive policy advocates during the upcoming Senate confirmation hearings.

The Road to Confirmation and Market Adaptation

In the short term, the market will remain hyper-sensitive to any rhetoric coming from the Senate Banking Committee. The confirmation hearings are expected to be contentious, as lawmakers grill Warsh on his willingness to let the market "self-correct" during periods of volatility. Investors should prepare for continued turbulence in the 10-year yield and the currency markets as the "Warshian" framework is stress-tested by real-world economic data.

Strategically, corporations are already beginning to pivot. Companies that spent the last decade optimized for a low-rate, high-liquidity environment are now forced to deleverage or find ways to boost margins through technology. This creates a market opportunity for "efficiency consultants" and AI integrators, while posing a challenge for "zombie firms" that have survived only through the grace of low interest rates. If Warsh is successful, the market may transition from a "liquidity-driven" rally to a "productivity-driven" bull market, though the path there is likely to be paved with volatility.

Potential scenarios range from a "Goldilocks" outcome—where AI indeed keeps inflation low while the Fed successfully shrinks its footprint—to a more chaotic "liquidity crunch" if the balance sheet reduction happens too quickly for the banking system to absorb. The next six months will be a critical testing ground for whether the private sector is truly ready to fly without the Fed’s training wheels.

Closing Thoughts: A Landmark Shift

The "Warsh Shock" represents one of the most significant pivots in the history of the Federal Reserve. By choosing a leader who prioritizes a leaner balance sheet and market-led growth, the administration has signaled a clear departure from the interventionist policies of the past. The immediate pain in the gold and crypto markets is a testament to how deeply the "debasement" mindset had taken root in the global consciousness.

Moving forward, the market will be defined by a return to fundamentals. Investors will no longer be able to rely on a central bank rescue for every 10% dip in the S&P 500. Instead, they must focus on companies with strong balance sheets, genuine productivity advantages, and the ability to thrive in a "sound money" environment. The "Warsh Shock" was a wake-up call; the coming months will determine who has the strength to stay awake.

Investors should closely watch the 10-year Treasury yield and the pace of the Fed’s MBS divestment. These will be the primary indicators of how aggressively the "Warshian" agenda is being implemented and whether the market’s plumbing can handle the transition to a leaner, more disciplined Federal Reserve.

This content is intended for informational purposes only and is not financial advice.